Two Sample t-test

data: mathematicians and accountants

t = 0.46359, df = 21, p-value = 0.6477

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.569496 10.338727

sample estimates:

mean of x mean of y

53.50000 51.61538 Statistical Models

Lecture 6

Lecture 6:

Two-sample

hypothesis tests

Outline of Lecture 6

- Two-sample hypothesis tests

- Two-sample t-test

- Two-sample t-test: Example

- Two-sample F-test

- Two-sample F-test: Example

Part 1:

Two-sample

hypothesis tests

Overview

In Lecture 4:

- Looked at data before and after the 2008 crash

- In this case data for each month is directly comparable

- Can then construct the difference between the 2007 and 2009 values

- Analysis reduces from a two-sample to a one-sample problem

Question

How do we analyze two samples that cannot be paired?

Problem statement

Goal: compare mean and variance of 2 independent samples

- First sample:

- Sample size n, sample mean \overline{x}, sample variance s^2_X

- Second sample:

- Sample size m, sample mean \overline{y}, sample variance s^2_Y

- We may have n \neq m

- Samples cannot be paired!

Tests available:

- Two-sample t-test to test for difference in means

- Two-sample F-test to test for difference in variances

Why is this important?

Hypothesis testing starts to get interesting with 2 or more samples

t-test and F-test show the normal distribution family in action

This is also the maths behind regression

- Same methods apply to seemingly unrelated problems

- Regression is a big subject in statistics

Normal distribution family in action

Two-sample t-test

- Want to compare the means of two independent samples

- At the same time population variances are unknown

- Therefore both variances are estimated with sample variances

- Test statistic is t_k-distributed with k linked to the total number of observations

Normal distribution family in action

Two-sample F-test

Want to compare the variance of two independent samples

This can be done by studying the ratio of the sample variances s^2_X/s^2_Y

We have already shown that \frac{(n - 1) S^2_X}{\sigma^2_X} \sim \chi^2_{n - 1} \qquad \frac{(m - 1) S^2_Y}{\sigma^2_Y} \sim \chi^2_{m - 1}

Normal distribution family in action

Two-sample F-test

Hence we can study statistic F = \frac{S^2_X / \sigma_X^2}{S^2_Y / \sigma_Y^2}

We will see that F has F-distribution

Part 2:

Two-sample t-test

The two-sample t-test

Assumptions: Suppose given samples from 2 normal populations

- X_1, \ldots ,X_n iid with distribution N(\mu_X,\sigma^2)

- Y_1, \ldots ,Y_m iid with distribution N(\mu_Y,\sigma^2)

Further assumptions:

- In general n \neq m so that one-sample t-test cannot be applied

- The two populations have same variance \sigma^2_X = \sigma^2_Y = \sigma^2

Note: Assuming same variance is simplification. Removing it leads to Welch t-test

The two-sample t-test

Goal: Compare means \mu_X and \mu_Y. We consider test H_0 \colon \mu_X = \mu_Y \qquad H_1 \colon \mu_X \neq \mu_Y

t-statistic: The general form is T = \frac{\text{Estimate}-\text{Hypothesised value}}{\text{e.s.e.}}

The two-sample t-statistic

Define the sample means \overline{X} = \frac{1}{n} \sum_{i=1}^n X_i \qquad \qquad \overline{Y} = \frac{1}{m} \sum_{i=1}^m Y_i

Notice that {\rm I\kern-.3em E}[ \overline{X} ] = \mu_X \qquad \qquad {\rm I\kern-.3em E}[ \overline{Y} ] = \mu_Y

Therefore we can estimate \mu_X - \mu_Y with the sample means, that is, \text{Estimate} = \overline{X} - \overline{Y}

The two-sample t-statistic

Since we are testing for difference in mean, we have \text{Hypothesised value} = \mu_X - \mu_Y

The Estimated Standard Error is the standard deviation of estimator \text{e.s.e.} = \text{Standard Deviation of } \overline{X} -\overline{Y}

The two-sample t-statistic

Therefore the two-sample t-statistic is T = \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{\text{e.s.e.}}

Under the Null Hypothesis that \mu_X = \mu_Y the t-statistic becomes T = \frac{\overline{X} - \overline{Y} }{\text{e.s.e.}}

A note on the degrees of freedom (df)

The general rule is \text{df} = \text{Sample size} - \text{No. of estimated parameters}

Sample size in two-sample t-test:

- n in the first sample

- m in the second sample

- Hence total number of observations is n + m

No. of estimated parameters is 2: Namely \mu_X and \mu_Y

Hence degree of freedoms in two-sample t-test is {\rm df} = n + m - 2

The estimated standard error

Recall: We are assuming populations have same variance \sigma^2_X = \sigma^2_Y = \sigma^2

We need to compute the estimated standard error \text{e.s.e.} = \text{Standard Deviation of } \ \overline{X} -\overline{Y}

Variance of sample mean was computed in the Lemma in Slide 17 Lecture 3

Since \overline{X} \sim N(\mu_X,\sigma^2) and \overline{Y} \sim N(\mu_Y,\sigma^2), by the Lemma we get {\rm Var}[\overline{X}] = \frac{\sigma^2}{n} \,, \qquad \quad {\rm Var}[\overline{Y}] = \frac{\sigma^2}{m}

The estimated standard error

Since X_i and Y_i are independent we get {\rm Cov}(X_i,Y_j)=0

By bilinearity of covariance we infer {\rm Cov}( \overline{X} , \overline{Y} ) = \frac{1}{n \cdot m} \sum_{i=1}^n \sum_{j=1}^m {\rm Cov}(X_i,Y_j) = 0

We can then compute \begin{align*} {\rm Var}[ \overline{X} - \overline{Y} ] & = {\rm Var}[ \overline{X} ] + {\rm Var}[ \overline{Y} ] - 2 {\rm Cov}( \overline{X} , \overline{Y} ) \\ & = {\rm Var}[ \overline{X} ] + {\rm Var}[ \overline{Y} ] \\ & = \sigma^2 \left( \frac{1}{n} + \frac{1}{m} \right) \end{align*}

The estimated standard error

Taking the square root gives \text{S.D.}(\overline{X} - \overline{Y} )= \sigma \ \sqrt{\frac{1}{n}+\frac{1}{m}}

Thus the form of the t-statistic becomes T = \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{\text{e.s.e.}} = \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{\sigma \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}}

Estimating the variance

The t-statistic is currently T = \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{\sigma \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}}

Variance \sigma^2 is unknown: need to estimate it

Define the sample variances

S_X^2 = \frac{ \sum_{i=1}^n X_i^2 - n \overline{X}^2 }{n-1} \qquad \qquad S_Y^2 = \frac{ \sum_{i=1}^m Y_i^2 - m \overline{Y}^2 }{m-1}

Estimating the variance

Recall that X_1, \ldots , X_n \sim N(\mu_X, \sigma^2) \qquad \qquad Y_1, \ldots , Y_m \sim N(\mu_Y, \sigma^2)

From Lecture 3 we know that S_X^2 and S_Y^2 are unbiased estimators of \sigma^2, e.g. {\rm I\kern-.3em E}[ S_X^2 ] = {\rm I\kern-.3em E}[ S_Y^2 ] = \sigma^2

Therefore both S_X^2 and S_Y^2 can be used to estimate \sigma^2

Estimating the variance

We can improve the estimate of \sigma^2 by combining S_X^2 and S_Y^2

We will consider a (convex) linear combination S^2 := \lambda_X S_X^2 + \lambda_Y S_Y^2 \,, \qquad \lambda_X + \lambda_Y = 1

S^2 is still an unbiased estimator of \sigma^2 since \begin{align*} {\rm I\kern-.3em E}[S^2] & = {\rm I\kern-.3em E}[ \lambda_X S_X^2 + \lambda_Y S_Y^2 ] \\ & = \lambda_X {\rm I\kern-.3em E}[S_X^2] + \lambda_Y {\rm I\kern-.3em E}[S_Y^2] \\ & = (\lambda_X + \lambda_Y) \sigma^2 \\ & = \sigma^2 \end{align*}

Estimating the variance

We choose coefficients \lambda_X and \lambda_Y that reflect sample sizes \lambda_X := \frac{n - 1}{n + m - 2} \qquad \qquad \lambda_Y := \frac{m - 1}{n + m - 2}

Notes:

We have \lambda_X + \lambda_Y = 1

Denominators in \lambda_X and \lambda_Y are degrees of freedom {\rm df } = n + m - 2

This choice is made so that S^2 has chi-squared distribution (more on this later)

Pooled estimator of variance

Definition

The pooled estimator of \sigma^2 is defined as

S_p^2 := \lambda_X S_X^2 + \lambda_Y S_Y^2

= \frac{(n-1) S_X^2 + (m-1) S_Y^2}{n + m - 2}

Note:

- n=m implies \lambda_X = \lambda_Y

- In this case S_X^2 and S_Y^2 have same weight in S_p^2

The two-sample t-statistic

The t-statistic has currently the form T = \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{\sigma \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}}

We replace \sigma with the pooled estimator S_p

The two-sample t-statistic

Definition

The two sample t-statistic is defined as

T := \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{ S_p \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}}

Note: Under the Null Hypothesis that \mu_X = \mu_Y this becomes T = \frac{\overline{X} - \overline{Y}}{ S_p \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}} = \frac{\overline{X} - \overline{Y}}{ \sqrt{ \dfrac{ (n-1) S_X^2 + (m-1) S_Y^2 }{n + m - 2} } \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}}

Distribution of two-sample t-statistic

Theorem

The two sample t-statistic has t_{n+m-2} distribution

T := \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{ S_p \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}} \sim t_{n + m - 2}

Distribution of two-sample t-statistic

Proof

We have already seen that \overline{X} - \overline{Y} is normal with {\rm I\kern-.3em E}[\overline{X} - \overline{Y}] = \mu_X - \mu_Y \qquad \qquad {\rm Var}[\overline{X} - \overline{Y}] = \sigma^2 \left( \frac{1}{n} + \frac{1}{m} \right)

Therefore we can rescale \overline{X} - \overline{Y} to get U := \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{ \sigma \sqrt{ \dfrac{1}{n} + \dfrac{1}{m}}} \sim N(0,1)

Distribution of two-sample t-statistic

Proof

We are assuming X_1, \ldots, X_n iid N(\mu_X,\sigma^2)

Therefore, as already shown, we have \frac{ (n-1) S_X^2 }{ \sigma^2 } \sim \chi_{n-1}^2

Similarly, since Y_1, \ldots, Y_m iid N(\mu_Y,\sigma^2), we get \frac{ (m-1) S_Y^2 }{ \sigma^2 } \sim \chi_{m-1}^2

Distribution of two-sample t-statistic

Proof

Since X_i and Y_j are independent, we also have that \frac{ (n-1) S_X^2 }{ \sigma^2 } \quad \text{ and } \quad \frac{ (m-1) S_Y^2 }{ \sigma^2 } \quad \text{ are independent}

In particular we obtain \frac{ (n-1) S_X^2 }{ \sigma^2 } + \frac{ (m-1) S_Y^2 }{ \sigma^2 } \sim \chi_{n-1}^2 + \chi_{m-1}^2 \sim \chi_{m + n- 2}^2

Distribution of two-sample t-statistic

Proof

Recall the definition of S_p^2 S_p^2 = \frac{(n-1) S_X^2 + (m-1) S_Y^2}{ n + m - 2 }

Therefore V := \frac{ (n+m-2) S_p^2 }{ \sigma^2 } = \frac{ (n - 1) S_X^2}{ \sigma^2} + \frac{ (m-1) S_Y^2 }{ \sigma^2 } \sim \chi_{n + m - 2}^2

Distribution of two-sample t-statistic

Proof

- Rewrite T as \begin{align*} T & = \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{ S_p \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}} \\ & = \frac{\overline{X} - \overline{Y} - (\mu_X - \mu_Y)}{ \sigma \sqrt{ \dfrac{1}{n} + \dfrac{1}{m} } } \Bigg/ \sqrt{ \frac{ (n + m - 2) S_p^2 \big/ \sigma^2}{ (n+ m - 2) } } \\ & = \frac{U}{\sqrt{V/(n+m-2)}} \end{align*}

Distribution of two-sample t-statistic

Proof

By construction \overline{X}- \overline{Y} is independent of S_X^2 and S_Y^2

Therefore \overline{X}- \overline{Y} is independent of S_p^2

We conclude that U and V are independent

We have shown that T = \frac{U}{\sqrt{V/(n+m-2)}} \,, \qquad U \sim N(0,1) \,, \qquad V \sim \chi_{n + m - 2}^2

By the Theorem in Slide 66 of Lecture 3 we conclude that T \sim t_{n+m-2}

The two-sample t-test

Procedure

Suppose given two independent samples

- Sample x_1, \ldots, x_n from N(\mu_X,\sigma^2) of size n

- Sample y_1, \ldots, y_m from N(\mu_Y,\sigma^2) of size m

The two-sided hypothesis test for difference in means is H_0 \colon \mu_X = \mu_Y \quad \qquad H_1 \colon \mu_X \neq \mu_Y

The two-sample t-test consists of 3 steps

The two-sample t-test

Procedure

- Calculation: Compute the two-sample t-statistic t = \frac{ \overline{x} - \overline{y}}{ s_p \ \sqrt{ \dfrac{1}{n} + \dfrac{1}{m} }} where sample means and pooled variance estimator are \overline{x} = \frac{1}{n} \sum_{i=1}^n x_i \qquad \overline{y} = \frac{1}{m} \sum_{i=1}^m y_i \qquad s_p^2 = \frac{ (n-1) s_X^2 + (m - 1) s_Y^2 }{ m + n - 2} s_X^2 = \frac{\sum_{i=1}^n x_i^2 - n \overline{x}^2}{n-1} \qquad s_Y^2 = \frac{\sum_{i=1}^m y_i^2 - m \overline{y}^2}{m-1}

The two-sample t-test

Procedure

- Statistical Tables or R: Find either

- Critical value in Table 13.1 t_{n + m - 2} (0.025)

- p-value in R p := 2 P( t_{n + m -2} > |t| )

The two-sample t-test

Procedure

- Interpretation:

- Reject H_0 if |t| > t_{n + m - 2} (0.025) \qquad \text{ or } \qquad p < 0.05

- Do not reject H_0 if |t| \leq t_{n + m - 2} (0.025) \qquad \text{ or } \qquad p \geq 0.05

The two-sample t-test in R

General commands

- Store the samples x_1,\ldots,x_n and y_1,\ldots,y_m in two R vectors

x_sample <- c(x1, ..., xn)y_sample <- c(y1, ..., ym)

- Perform a two-sided two-sample t-test on

x_sampleandy_samplet.test(x_sample, y_sample, var.equal = TRUE)

- Read output

- Output is similar to one-sample t-test

- The main quantity of interest is p-value

t-test command options

Comments on command t.test(x, y)

R will perform a two-sample t-test on populations

xandyR implicitly assumes the null hypothesis is H_0 \colon \mu_X = \mu_Y

mu = mu0tells R to test null hypothesis: H_0 \colon \mu_X = \mu_Y + \mu_0

t-test command options

Comments on command t.test(x, y)

- One-sided two sample t-test can be performed by specifying

alternative = "greater"which tests H_1 \colon \mu_X > \mu_Y + \mu_0alternative = "smaller"which tests H_1 \colon \mu_X < \mu_Y + \mu_0

t-test command options

Comments on command t.test(x, y)

var.equal = TRUEtells R to assume that populations have same variance \sigma_X^2 = \sigma^2_YIn this case R computes the t-statistic with formula discussed earlier t = \frac{ \overline{x} - \overline{y} }{s_p \sqrt{ \dfrac{1}{n} + \dfrac{1}{m} }}

t-test command options

Comments on command t.test(x, y)

Warning: If var.equal = TRUE is not specified then

R assumes that populations have different variance \sigma_X^2 \neq \sigma^2_Y

In this case the t-statistic t = \frac{ \overline{x} - \overline{y} }{s_p \sqrt{ \dfrac{1}{n} + \dfrac{1}{m} }} is NOT t-distributed

R performs the Welch t-test instead of the classic t-test

t-test command options

Comments on command t.test(x, y)

- Welch t-test consists in computing the Welch statistic w = \frac{\overline{x} - \overline{y}}{ \sqrt{ \dfrac{s_X^2}{n} + \dfrac{s_Y^2}{m} } }

- If sample sizes m,n > 5 then w is approximately t-distributed

- Degrees of freedom are not integer, and depend on S_X, S_Y, n, m

Bottom line:

- p-value from Welch t-test is similar to p-value from two-sample t-test

- Since p-values are similar, most times the 2 tests yield same decision

Part 3:

Two-sample t-test

Example

Two-sample t-test

Example

Samples: Wage data on 10 Mathematicians and 13 Accountants

Assumptions: Wages are independent and normally distributed

Goal: Compare mean wage for the 2 professions

- Is there evidence of differences in average pay?

| Mathematicians | x_1 | x_2 | x_3 | x_4 | x_5 | x_6 | x_7 | x_8 | x_9 | x_{10} |

|---|---|---|---|---|---|---|---|---|---|---|

| Wages | 36 | 40 | 46 | 54 | 57 | 58 | 59 | 60 | 62 | 63 |

| Accountants | y_1 | y_2 | y_3 | y_4 | y_5 | y_6 | y_7 | y_8 | y_9 | y_{10} | y_{11} | y_{12} | y_{13} |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Wages | 37 | 37 | 42 | 44 | 46 | 48 | 54 | 56 | 59 | 60 | 60 | 64 | 64 |

Calculations: First sample

Sample size: \ n = No. of Mathematicians = 10

Mean: \bar{x} = \frac{\sum_{i=1}^n x_i}{n} = \frac{36+40+46+ \ldots +62+63}{10}=\frac{535}{10}=53.5

Variance: \begin{align*} s^2_X & = \frac{\sum_{i=1}^n x_i^2 - n \bar{x}^2}{n -1 } \\ \sum_{i=1}^n x_i^2 & = 36^2+40^2+46^2+ \ldots +62^2+63^2 = 29435 \\ s^2_X & = \frac{29435-10(53.5)^2}{9} = 90.2778 \end{align*}

Calculations: Second sample

Sample size: \ m = No. of Accountants = 13

Mean: \bar{y} = \frac{37+37+42+ \dots +64+64}{13} = \frac{671}{13} = 51.6154

Variance: \begin{align*} s^2_Y & = \frac{\sum_{i=1}^m y_i^2 - m \bar{y}^2}{m - 1} \\ \sum_{i=1}^m y_i^2 & = 37^2+37^2+42^2+ \ldots +64^2+64^2 = 35783 \\ s^2_Y & = \frac{35783-13(51.6154)^2}{12} = 95.7547 \end{align*}

Calculations: Pooled Variance

Pooled variance: \begin{align*} s_p^2 & = \frac{(n-1) s_X^2 + (m-1) s_Y^2}{ n + m - 2} \\ & = \frac{(9) 90.2778 + (12) 95.7547 }{ 10 + 13 - 2} \\ & = 93.40746 \end{align*}

Pooled standard deviation: s_p = \sqrt{93.40746} = 9.6648

Calculations: t-statistic

- Calculation: Compute the two-sample t-statistic

\begin{align*} t & = \frac{\bar{x} - \bar{y} }{s_p \ \sqrt{\dfrac{1}{n}+\dfrac{1}{m}}} \\ & = \frac{53.5 - 51.6154}{9.6648 \times \sqrt{\dfrac{1}{10}+\dfrac{1}{13}}} \\ & = \frac{1.8846}{9.6648{\times}0.4206} \\ & = 0.464 \,\, (3\ \text{d.p.}) \end{align*}

Completing the t-test

- Referencing Tables:

- Degrees of freedom = n + m - 2 = 10 + 13 - 2 = 21

- Find corresponding critical value in Table 13.1 t_{21}(0.025) = 2.08

Completing the t-test

- Interpretation:

We have that | t | = 0.464 < 2.08 = t_{21}(0.025)

Therefore the p-value satisfies p>0.05

There is no evidence (p>0.05) in favor of H_1

Hence we accept that \mu_X = \mu_Y

- Conclusion: Average pay levels seem to be the same for both professions

The two-sample t-test in R: Code

# Enter Wages data in 2 vectors using function c()

mathematicians <- c(36, 40, 46, 54, 57, 58, 59, 60, 62, 63)

accountants <- c(37, 37, 42, 44, 46, 48, 54, 56, 59, 60, 60, 64, 64)

# Perform two-sample t-test with null hypothesis mu_X = mu_Y

# Specify that populations have same variance

# Store result of t.test in answer

answer <- t.test(mathematicians, accountants, var.equal = TRUE)

# Print answer

print(answer)- Code can be downloaded here two_sample_t_test.R

The two-sample t-test in R: Output

Comments:

- First line: R tells us that a Two-Sample t-test is performed

- Second line: Data for t-test is

mathematiciansandaccountants

The two-sample t-test in R: Output

Two Sample t-test

data: mathematicians and accountants

t = 0.46359, df = 21, p-value = 0.6477

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.569496 10.338727

sample estimates:

mean of x mean of y

53.50000 51.61538 Comments:

- The t-statistic computed is t = 0.46359

- Note: This coincides with the one computed by hand

- There are 21 degrees of freedom and p-value is p = 0.6477

The two-sample t-test in R: Output

Two Sample t-test

data: mathematicians and accountants

t = 0.46359, df = 21, p-value = 0.6477

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.569496 10.338727

sample estimates:

mean of x mean of y

53.50000 51.61538 Comments:

- Fourth line: The alternative hypothesis is that the difference in means is not zero

- This translates to H_1 \colon \mu_X \neq \mu_Y

- Warning: This is not saying to reject H_0 – R is just stating H_1

The two-sample t-test in R: Output

Two Sample t-test

data: mathematicians and accountants

t = 0.46359, df = 21, p-value = 0.6477

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.569496 10.338727

sample estimates:

mean of x mean of y

53.50000 51.61538 Comments:

- Fifth line: R computes a 95 \% confidence interval for \mu_X - \mu_Y

- Based on the data, the set of hypothetical values for \mu_X - \mu_Y is (\mu_X - \mu_Y) \in [-6.569496, 10.338727]

The two-sample t-test in R: Output

Two Sample t-test

data: mathematicians and accountants

t = 0.46359, df = 21, p-value = 0.6477

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.569496 10.338727

sample estimates:

mean of x mean of y

53.50000 51.61538 Comments:

- Seventh line: R computes sample mean for the two populations

- Sample mean for

mathematiciansis 53.5 - Sample mean for

accountantsis 51.61538

- Sample mean for

The two-sample t-test in R: Output

Two Sample t-test

data: mathematicians and accountants

t = 0.46359, df = 21, p-value = 0.6477

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.569496 10.338727

sample estimates:

mean of x mean of y

53.50000 51.61538 Conclusion: The p-value is p = 0.6477

- Since p > 0.05 we do not reject H_0

- Hence \mu_X and \mu_Y appear to be similar

- Average pay levels seem to be the same for both professions

t-test without assuming same variance

In the previous t-tests we assumed the populations have same variance \sigma_X^2 = \sigma_Y^2

R can also perform t-test without assuming \sigma_X^2 = \sigma_Y^2

- This is called Welch Two-sample t-test

- It can be performed with

t.test(x, y) - Note that we are omitting the option

var.equal = TRUE

t-test without assuming same variance

Warnings:

The p-value obtained with Welch t-test is usually comparable to the one obtained with classic t-test

The t-statistic of Welch t-test is different from the one of the classic t-test

- Indeed Welch t-test and classic t-test compute statistics, respectively, w = \frac{\overline{x} - \overline{y}}{ \sqrt{ \dfrac{s_X^2}{n} + \dfrac{s_Y^2}{m} } } \qquad \qquad t = \frac{ \overline{x} - \overline{y} }{s_p \sqrt{ \dfrac{1}{n} + \dfrac{1}{m} }}

Welch two-sample t-test: Code

# Enter Wages data in 2 vectors using function c()

mathematicians <- c(36, 40, 46, 54, 57, 58, 59, 60, 62, 63)

accountants <- c(37, 37, 42, 44, 46, 48, 54, 56, 59, 60, 60, 64, 64)

# Perform Welch two-sample t-test with null hypothesis mu_X = mu_Y

# Store result of t.test in answer

answer <- t.test(mathematicians, accountants)

# Print answer

print(answer)- Note:

- This is almost the same code as in Slide 48

- We are only omitting the option

var.equal = TRUEint.test

Welch two-sample t-test: Output

Welch Two Sample t-test

data: mathematicians and accountants

t = 0.46546, df = 19.795, p-value = 0.6467

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.566879 10.336109

sample estimates:

mean of x mean of y

53.50000 51.61538 Comments:

- First line: R tells us that a Welch Two-Sample t-test is performed

- The rest of the output is similar to classic t-test

- Main difference is that p-value and t-statistic differ from classic t-test

Welch two-sample t-test: Output

Welch Two Sample t-test

data: mathematicians and accountants

t = 0.46546, df = 19.795, p-value = 0.6467

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.566879 10.336109

sample estimates:

mean of x mean of y

53.50000 51.61538 Comments:

- Also note that degrees of freedom are fractionary:

- This is because the Welch statistic is approximately t-distributed

- In this example it can be approximated with t_{n} with n = 19.795

Welch two-sample t-test: Output

Welch Two Sample t-test

data: mathematicians and accountants

t = 0.46546, df = 19.795, p-value = 0.6467

alternative hypothesis: true difference in means is not equal to 0

95 percent confidence interval:

-6.566879 10.336109

sample estimates:

mean of x mean of y

53.50000 51.61538 Conclusion: The p-values obtained with the 2 tests are very similar

- Welch t-test: p-value = 0.6467

- Classic t-test: p-value = 0.6477

- Both test: p > 0.05 and therefore do not reject H_0

Part 4:

Two-sample F-test

Variance estimators

Suppose given random samples from 2 normal populations:

- X_1, \ldots, X_n iid random sample from N(\mu_X, \sigma_X^2)

- Y_1, \ldots, Y_m iid random sample from N(\mu_Y, \sigma_Y^2)

Problem:

- We want to compare variance of the 2 populations

- A way to do it is by estimating the variances ratio \frac{\sigma_X^2}{\sigma_Y^2}

Variance estimators

Question:

- Suppose the variances \sigma_X^2 and \sigma_Y^2 are unknown

- How can we estimate the ratio \sigma_X^2 /\sigma_Y^2 \, ?

Answer:

Estimate the ratio \sigma_X^2 /\sigma_Y^2 \, using sample variances S^2_X / S^2_Y

The F-distribution allows to compare the quantities \sigma_X^2 /\sigma_Y^2 \qquad \text{and} \qquad S^2_X / S^2_Y

Variance ratio distribution

Theorem

Suppose given random samples from 2 normal populations:

- X_1, \ldots, X_n iid random sample from N(\mu_X, \sigma_X^2)

- Y_1, \ldots, Y_m iid random sample from N(\mu_Y, \sigma_Y^2)

The random variable F = \frac{ S_X^2 / \sigma_X^2 }{ S_Y^2 / \sigma_Y^2 } has F-distribution with n-1 and m-1 degrees of freedom.

Variance ratio distribution

Proof

We need to prove F = \frac{ S_X^2 / \sigma_X^2 }{ S_Y^2 / \sigma_Y^2 } \sim F_{n-1,m-1}

By the Theorem in Slide 48 Lecture 3 we have that \frac{S_X^2}{ \sigma_X^2} \sim \frac{\chi_{n-1}^2}{n-1} \,, \qquad \frac{S_Y^2}{ \sigma_Y^2} \sim \frac{\chi_{m-1}^2}{m-1}

Variance ratio distribution

Proof

Therefore F = \frac{ S_X^2 / \sigma_X^2 }{ S_Y^2 / \sigma_Y^2 } = \frac{U/p}{V/q} where we have U \sim \chi_{p}^2 \,, \qquad V \sim \chi_q^2 \,, \qquad p = n-1 \,, \qquad q = m - 1

By the Theorem in Slide 46 Lecture 5 we infer the thesis F = \frac{U/p}{V/q} \sim F_{n-1,m-1}

Unbiased estimation of variance ratio

Question: Why is S_X^2/S_Y^2 a good estimator of \sigma_X^2/\sigma_Y^2

Answer:

- Because S_X^2/S_Y^2 is (asymptotically) unbiased estimator of \sigma_X^2/\sigma_Y^2

- This is shown in the following Theorem

Unbiased estimation of variance ratio

Theorem

Suppose given independent random samples from 2 normal populations:

- X_1, \ldots, X_n iid random sample from N(\mu_X, \sigma_X^2)

- Y_1, \ldots, Y_m iid random sample from N(\mu_Y, \sigma_Y^2)

It holds that {\rm I\kern-.3em E}\left[ \frac{S_X^2}{S_Y^2} \right] = \frac{m-1}{m-3} \frac{\sigma_X^2}{\sigma_Y^2} \,, \qquad \lim_{m \to \infty} {\rm I\kern-.3em E}\left[ \frac{S_X^2}{S_Y^2} \right] = \frac{\sigma_X^2}{\sigma_Y^2}

Proof: Will be left as an exercise

Two-sample one-sided F-test

Assumptions: Suppose given samples from 2 normal populations

- X_1, \ldots, X_n iid with distribution N(\mu_X, \sigma_X^2)

- Y_1, \ldots, Y_m iid with distribution N(\mu_Y, \sigma_Y^2)

Goal: Compare variances \sigma_X^2 and \sigma_Y^2. We consider the test H_0 \colon \sigma_X^2 = \sigma_Y^2 \qquad \qquad H_1 \colon \sigma_X^2 > \sigma_Y^2

Two-sample one-sided F-test

Statistic: For the variance test we will use the F-statistic F = \frac{ S_X^2 / \sigma_X^2 }{ S_Y^2 / \sigma_Y^2 } \sim F_{n-1,m-1}

Note: Under the Null hypothesis that \sigma_X^2 = \sigma_Y^2 the F-statistic simplifies to F = \frac{ S_X^2 }{ S_Y^2 } \sim F_{n-1,m-1}

Computing F-statistic with tables

F-distribution tables are often one-sided

This is because, in general, F-tests associated with regression are one-sided tests

This means that in our hand calculation examples we construct F-statistic as F = \frac{s^2_X}{s^2_Y} \quad\quad \text{where} \quad\quad s^2_X > s^2_Y

The above guarantees F>1 and we can use one-sided F-tables

Computing F-statistic with tables

- F-distribution probabilities are in Tables 13.2 and 13.3 of Statistics_Tables.pdf

The values F_{\nu_1,\nu_2}(0.05) listed are such that P(F_{\nu_1,\nu_2} > F_{\nu_1,\nu_2}(0.05)) = 0.05

For example F_{4,3}(0.05) = 9.12

Computing F-statistic with tables

Sometimes the value F_{\nu_1,\nu_2}(0.05) is missing from F-table

In such case approximate F_{\nu_1,\nu_2}(0.05) with average of closest entries available

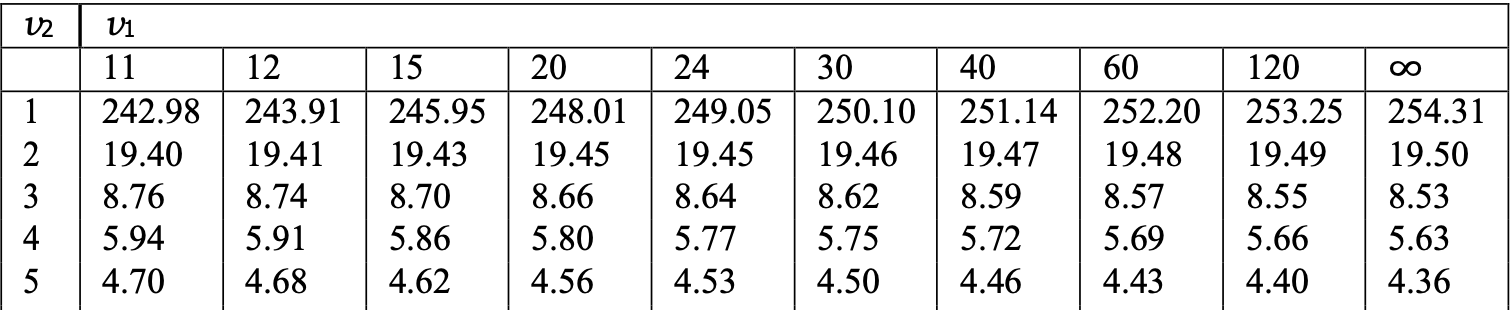

- Example: F_{21,5}(0.05) is missing. We can approximate it by F_{21,5}(0.05) \approx \frac{F_{20,5}(0.05) + F_{24,5}(0.05)}{2} = \frac{ 4.56 + 4.53 }{ 2 } = 4.545

The two-sample F-test

Procedure

Suppose given two independent samples

- sample x_1, \ldots, x_n from N(\mu_X,\sigma^2) of size n

- sample y_1, \ldots, y_m from N(\mu_Y,\sigma^2) of size m

The one-sided hypothesis test for difference in variances is H_0 \colon \sigma^2_X = \sigma^2_Y \quad \qquad H_1 \colon \sigma^2_X > \sigma^2_Y

The two-sample F-test consists of 3 steps

The two-sample F-test

Procedure

- Calculation: Compute the two-sample F-statistic F = \frac{ s_X^2}{ s_Y^2} where sample variances are s_X^2 = \frac{\sum_{i=1}^n x_i^2 - n \overline{x}^2}{n-1} \qquad \quad s_Y^2 = \frac{\sum_{i=1}^m y_i^2 - m \overline{y}^2}{m-1}

- s_X^2 refers to sample with largest variance

- This way s_X^2 > s_Y^2, so that F > 1

The two-sample F-test

Procedure

- Statistical Tables or R: Find either

- Critical value in Tables 13.2, 13.3 F_{n-1,m-1} (0.05)

- p-value in R p := P( F_{n - 1, m-1} > |F| )

The two-sample F-test

Procedure

- Interpretation:

- Reject H_0 if |F| > F_{n - 1, m-1} (0.05) \qquad \text{ or } \qquad p < 0.05

- Do not reject H_0 if |F| \leq F_{n -1, m-1} (0.05) \qquad \text{ or } \qquad p \geq 0.05

The two-sample F-test in R

Procedure using var.test

- Store the samples x_1,\ldots,x_n and y_1,\ldots,y_m in two R vectors

x_sample <- c(x1, ..., xn)y_sample <- c(y1, ..., ym)

- Perform a two-sample one-sided F-test on

x_sampleandy_samplevar.test(x_sample, y_sample, alternative = "greater")

- Read output

- Output is similar to two-sample t-test

- The main quantity of interest is p-value

Note: alternative = "greater" specifies alternative hypothesis \sigma_X^2 > \sigma_Y^2

Part 5:

Two-sample F-test

Example

Two-sample F-test

Example

Samples: Back to example of wages of 10 Mathematicians and 13 Accountants

Assumptions: Wages are independent and normally distributed

Goal: Compare variance of wages for the 2 professions

- Is there evidence of differences in how spread out pays are?

| Mathematicians | x_1 | x_2 | x_3 | x_4 | x_5 | x_6 | x_7 | x_8 | x_9 | x_{10} |

|---|---|---|---|---|---|---|---|---|---|---|

| Wages | 36 | 40 | 46 | 54 | 57 | 58 | 59 | 60 | 62 | 63 |

| Accountants | y_1 | y_2 | y_3 | y_4 | y_5 | y_6 | y_7 | y_8 | y_9 | y_{10} | y_{11} | y_{12} | y_{13} |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Wages | 37 | 37 | 42 | 44 | 46 | 48 | 54 | 56 | 59 | 60 | 60 | 64 | 64 |

Calculations: First sample

Repeat calculations of Slide 43

Sample size: \ n = No. of Mathematicians = 10

Mean: \bar{x} = \frac{\sum_{i=1}^n x_i}{n} = \frac{36+40+46+ \ldots +62+63}{10}=\frac{535}{10}=53.5

Variance: \begin{align*} \sum_{i=1}^n x_i^2 & = 36^2+40^2+46^2+ \ldots +62^2+63^2 = 29435 \\ s^2_X & = \frac{\sum_{i=1}^n x_i^2 - n \bar{x}^2}{n -1 } = \frac{29435-10(53.5)^2}{9} = 90.2778 \end{align*}

Calculations: Second sample

Repeat calculations of Slide 44

Sample size: \ m = No. of Accountants = 13

Mean: \bar{y} = \frac{37+37+42+ \dots +64+64}{13} = \frac{671}{13} = 51.6154

Variance: \begin{align*} \sum_{i=1}^m y_i^2 & = 37^2+37^2+42^2+ \ldots +64^2+64^2 = 35783 \\ s^2_Y & = \frac{\sum_{i=1}^m y_i^2 - m \bar{y}^2}{m - 1} = \frac{35783-13(51.6154)^2}{12} = 95.7547 \end{align*}

Calculations: F-statistic

Calculation:

Notice that s^2_Y = 95.7547 > 90.2778 = s_X^2

Hence the F-statistic is F = \frac{s^2_Y}{s_X^2} = \frac{95.7547}{90.2778} = 1.061\ \quad (3\ \text{d.p.})

Note: We have swapped role of s^2_X and s^2_Y, since s^2_Y > s^2_X

Completing the F-test

- Referencing Tables:

Degrees of freedom are n - 1 = 10 - 1 = 9 \,, \qquad m - 1 = 13 - 1 = 12

Note: Since we have swapped role of s^2_X and s^2_Y, we have F = \frac{s^2_Y}{s_X^2} \sim F_{m-1,n-1} = F_{12,9}

Find corresponding critical value in Tables 13.2, 13.3 F_{12, 9}(0.05) = 3.07

Completing the F-test

- Interpretation:

- We have that F = 1.061 < 3.07 = F_{12, 9}(0.05)

- Therefore the p-value satisfies p > 0.05

- There is no evidence (p > 0.05) in favor of H_1

- Hence we accept that \sigma_X^2 = \sigma_Y^2

- Conclusion: Wage levels for the two groups appear to be equally well spread out

The F-test in R

We present two F-test solutions in R

- Simple solution using the command

var.test - A first-principles construction closer to our earlier hand calculation

Simple solution: Code

# Enter Wages data in 2 vectors using function c()

mathematicians <- c(36, 40, 46, 54, 57, 58, 59, 60, 62, 63)

accountants <- c(37, 37, 42, 44, 46, 48, 54, 56, 59, 60, 60, 64, 64)

# Perform one-sided F-test using var.test

# Store result of var.test in ans

ans <- var.test(accountants, mathematicians, alternative = "greater")

# Print answer

print(ans)- Note:

accountantsis first because it has larger variance - Code can be downloaded here F_test.R

Simple solution: Output

F test to compare two variances

data: accountants and mathematicians

F = 1.0607, num df = 12, denom df = 9, p-value = 0.4753

alternative hypothesis: true ratio of variances is greater than 1

95 percent confidence interval:

0.3451691 Inf

sample estimates:

ratio of variances

1.060686 Comments:

- First line: R tells us that an F-test is performed

- Second line: Data for F-test is

accountantsandmathematicians

Simple solution: Output

F test to compare two variances

data: accountants and mathematicians

F = 1.0607, num df = 12, denom df = 9, p-value = 0.4753

alternative hypothesis: true ratio of variances is greater than 1

95 percent confidence interval:

0.3451691 Inf

sample estimates:

ratio of variances

1.060686 Comments:

- The F-statistic computed is F = 1.0607

- Note: This coincides with the one computed by hand (up to rounding error)

Simple solution: Output

F test to compare two variances

data: accountants and mathematicians

F = 1.0607, num df = 12, denom df = 9, p-value = 0.4753

alternative hypothesis: true ratio of variances is greater than 1

95 percent confidence interval:

0.3451691 Inf

sample estimates:

ratio of variances

1.060686 Comments:

- Numerator of F-statistic has 12 degrees of freedom

- Denominator of F-statistic has 9 degrees of freedom

- p-value is p = 0.4753

Simple solution: Output

F test to compare two variances

data: accountants and mathematicians

F = 1.0607, num df = 12, denom df = 9, p-value = 0.4753

alternative hypothesis: true ratio of variances is greater than 1

95 percent confidence interval:

0.3451691 Inf

sample estimates:

ratio of variances

1.060686 Comments:

- Fourth line: The alternative hypothesis is that ratio of variances is \, > 1

- This translates to H_1 \colon \sigma_X^2 > \sigma^2_Y

- Warning: This is not saying to reject H_0 – R is just stating H_1

Simple solution: Output

F test to compare two variances

data: accountants and mathematicians

F = 1.0607, num df = 12, denom df = 9, p-value = 0.4753

alternative hypothesis: true ratio of variances is greater than 1

95 percent confidence interval:

0.3451691 Inf

sample estimates:

ratio of variances

1.060686 Comments:

- Fifth line: R computes a 95 \% confidence interval for ratio \sigma_Y^2/\sigma_X^2

- Based on the data, the set of hypothetical values for \sigma_Y^2/\sigma_X^2 is (\sigma_Y^2/\sigma_X^2 ) \in [0.3451691, \infty]

Simple solution: Output

F test to compare two variances

data: accountants and mathematicians

F = 1.0607, num df = 12, denom df = 9, p-value = 0.4753

alternative hypothesis: true ratio of variances is greater than 1

95 percent confidence interval:

0.3451691 Inf

sample estimates:

ratio of variances

1.060686 Comments:

- Seventh line: R computes ratio of sample variances

- We have that s_Y^2/s_X^2 = 1.060686

- By definition the above coincides with F-statistic (up to rounding)

Simple solution: Output

F test to compare two variances

data: accountants and mathematicians

F = 1.0607, num df = 12, denom df = 9, p-value = 0.4753

alternative hypothesis: true ratio of variances is greater than 1

95 percent confidence interval:

0.3451691 Inf

sample estimates:

ratio of variances

1.060686 Conclusion: The p-value is p = 0.4753

- Since p > 0.05 we do not reject H_0

- Hence \sigma^2_X and \sigma^2_Y appear to be similar

- Wage levels for the two groups appear to be equally well spread out

First principles solution: Code

- Start by entering data into R

First principles solution: Code

- Check which population has higher variance

- In our case

accountantshas higher variance

First principles solution: Code

- Compute sample sizes

First principles solution: Code

Compute F-statistic F = \frac{s_Y^2}{s_X^2}

Recall: Numerator has to have larger variance

In our case

accountantsis numerator

First principles solution: Code

- Compute the p-value p = P(F_{m-1, n-1} > F) = 1 - P(F_{m-1, n-1} \leq F)

# Compute p-value

p_value <- 1 - pf(F, df1 = m - 1, df2 = n - 1)

# Print p-value

cat("\n The p-value for one-sided F-test is", p_value)- Note: The command

pf(f, df1 = n, df2 = m)computes probability P(F_{n,m} \leq f)

First principles solution: Output

Full code be downloaded here F_test_first_principles.R

Running the code yields the output:

Variance of accountants is 95.75641

Variance of mathematicians is 90.27778

The p-value for one-sided F-test is 0.4752684- Since p > 0.05 we do not reject H_0