Part 3:

Basic question in regression

What happens to Y as X increases?

increases?

decreases?

nothing?

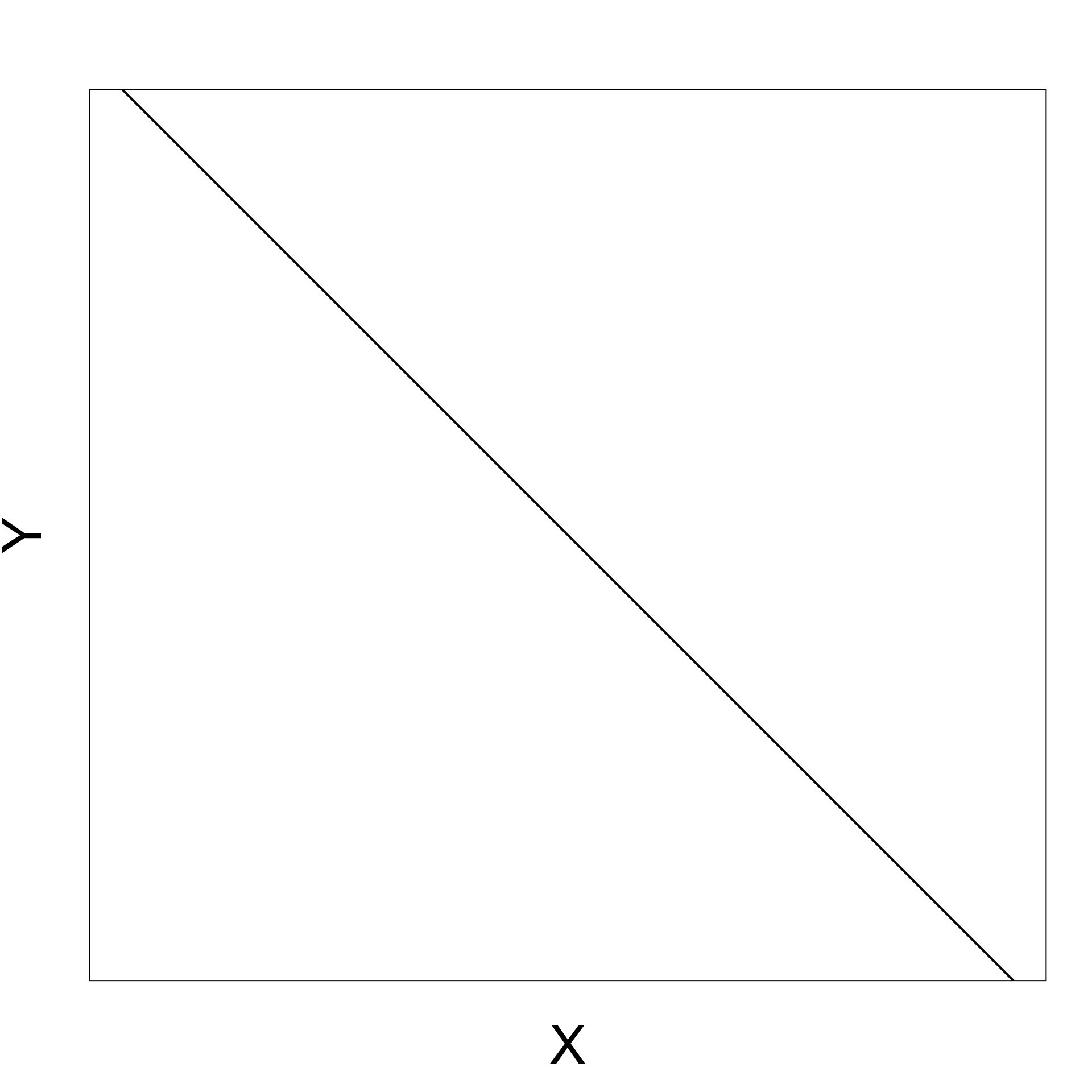

Positive gradient

As X increases Y increases

Negative gradient

As X increases Y decreases

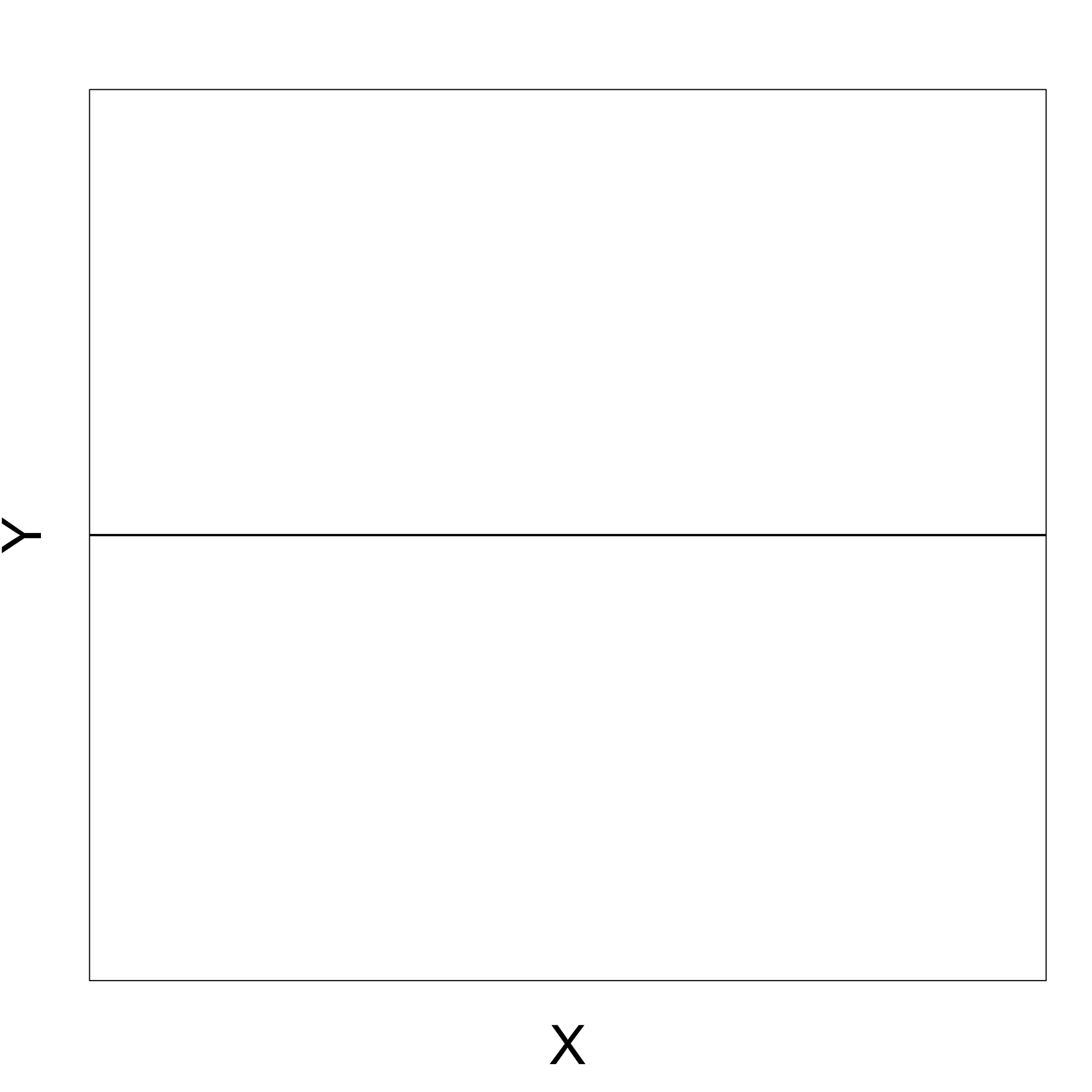

Zero gradient

Changes in X do not affect Y

t-test for simple regression

Consider the simple linear regression model

Y_i = \alpha + \beta X_i + \varepsilon_i

X \,\, \text{ affects } \,\, Y \qquad \iff \qquad

\beta \neq 0

\begin{align*}

H_0 \colon & \beta = b \\

H_1 \colon & \beta \neq b

\end{align*}

Construction of t-test

\begin{align*}

H_0 \colon & \beta = b \\

H_1 \colon & \beta \neq b

\end{align*}

Distribution of \hat \beta

Theorem Consider the linear regression model

Y_i = \alpha + \beta x_i + \varepsilon_i

with \varepsilon_i iid N(0, \sigma^2) . Then

\hat \beta \sim N \left(\beta , \frac{ \sigma^2 }{ S_{xx} } \right)

Proof: Quite difficult. If interested see Theorem 11.3.3 in [1 ]

Construction of the t-statistic

We want to construct t-statistic for \hat \beta

As for the standard t-test, we want a t-statistic of the form

t = \frac{\text{Estimate } - \text{ Hypothesised Value}}{\mathop{\mathrm{e.s.e.}}}

\hat \beta \sim N \left(\beta , \frac{ \sigma^2 }{ S_{xx} } \right)

Construction of the t-statistic

In particular \hat \beta is an unbiased estimator for \beta

{\rm I\kern-.3em E}[ \hat \beta ] = \beta

Therefore \hat \beta is the estimate

t = \frac{\text{Estimate } - \text{ Hypothesised Value}}{\mathop{\mathrm{e.s.e.}}}

= \frac{ \hat \beta - \beta }{ \mathop{\mathrm{e.s.e.}}}

Estimated Standard Error

{\rm Var}[\hat \beta] = \frac{ \sigma^2 }{ S_{xx}}

Hence the standard error of \hat \beta is the standard deviation

{\rm SD}[\hat \beta] = \frac{ \sigma }{ S_{xx} }

{\rm SD} cannot be used for testing, since \sigma^2 is unknown

Estimated Standard Error

We however have an estimate for \sigma^2

\hat \sigma^2 = \frac{1}{n} \mathop{\mathrm{RSS}}= \frac1n \sum_{i=1}^n (y_i - \hat y_i)^2

{\rm I\kern-.3em E}[ \hat\sigma^2 ] = \frac{n-2}{n} \, \sigma^2

Estimated Standard Error

S^2 := \frac{n}{n-2} \, \hat\sigma^2 = \frac{\mathop{\mathrm{RSS}}}{n-2}

This way S^2 is unbiased estimator for \sigma^2

{\rm I\kern-.3em E}[S^2] = \frac{n}{n-2} \, {\rm I\kern-.3em E}[\hat\sigma^2] = \frac{n}{n-2} \, \frac{n-2}{n} \, \sigma^2 = \sigma^2

Estimated Standard Error

Recall that the standard deviation of \hat \beta is

{\rm SD}[\hat \beta] = \frac{ \sigma }{ S_{xx} }

\mathop{\mathrm{e.s.e.}}= \frac{S}{\sqrt{S_{xx}}}

t-statistic to test \hat \beta

The t-statistic for \hat \beta is then

t = \frac{\text{Estimate } - \text{ Hypothesised Value}}{\mathop{\mathrm{e.s.e.}}}

= \frac{ \hat \beta - \beta }{ S / \sqrt{S_{xx}} }

Theorem Consider the linear regression model

Y_i = \alpha + \beta x_i + \varepsilon_i

with \varepsilon_i iid N(0, \sigma^2) . Then

t = \frac{ \hat \beta - \beta }{ S / \sqrt{S_{xx}} }

\, \sim \,

t_{n-2}

How to prove the Theorem

Proof of this Theorem is quite difficult and we omit it

If you are interested in the proof, see Section 11.3.4 in [1 ]

The main idea is that t-statistic can be rewritten as

t = \frac{ \hat \beta - \beta }{ S / \sqrt{S_{xx}} }

= \frac{ U }{ \sqrt{ V/(n-2) } }

U := \frac{ \hat \beta - \beta }{ \sigma / \sqrt{S_{xx}} } \,, \qquad \quad V := \frac{ (n-2) S^2 }{ \sigma^2 }

How to prove the Theorem

\hat \beta \sim N \left(\beta , \frac{ \sigma^2 }{ S_{xx} } \right)

U = \frac{ \hat \beta - \beta }{ \sigma / \sqrt{S_{xx}} } \, \sim \, N(0,1)

How to prove the Theorem

Moreover it can be shown that

V = \frac{(n-2) S^2}{\sigma^2} \, \sim \, \chi_{n-2}^2

It can also be shown that U and V are independent

How to prove the Theorem

t = \frac{ \hat \beta - \beta }{ S / \sqrt{S_{xx}} }

= \frac{ U }{ \sqrt{ V/(n-2) } }

U and V are independent, with

U \sim N(0,1) \,, \qquad \quad V \sim \chi_{n-2}^2

From the Theorem on t-distribution in Lecture 3 we conclude

t \sim t_{n-2}

Summary: t-test for \beta

Goal : Estimate the slope \beta for the simple linear model

Y_i = \alpha + \beta x_i + \varepsilon_i \,, \qquad \varepsilon_i \, \text{ iid } \, N(0,\sigma^2)

Hypotheses : If b is guess for \beta the hypotheses are

\begin{align*}

H_0 & \colon \beta = b \\

H_1 & \colon \beta \neq b

\end{align*}

Summary: t-test for \beta

t = \frac{\hat \beta - b }{ \mathop{\mathrm{e.s.e.}}} \, \sim \, t_{n-2} \,, \qquad \quad

\mathop{\mathrm{e.s.e.}}= \frac{S }{\sqrt{S_{xx}} }

\hat \beta = \frac{ S_{xy} }{ S_{xx} } \,, \qquad \quad S^2 := \frac{\mathop{\mathrm{RSS}}}{n-2}

p = 2 P( t_{n-2} > |t| )

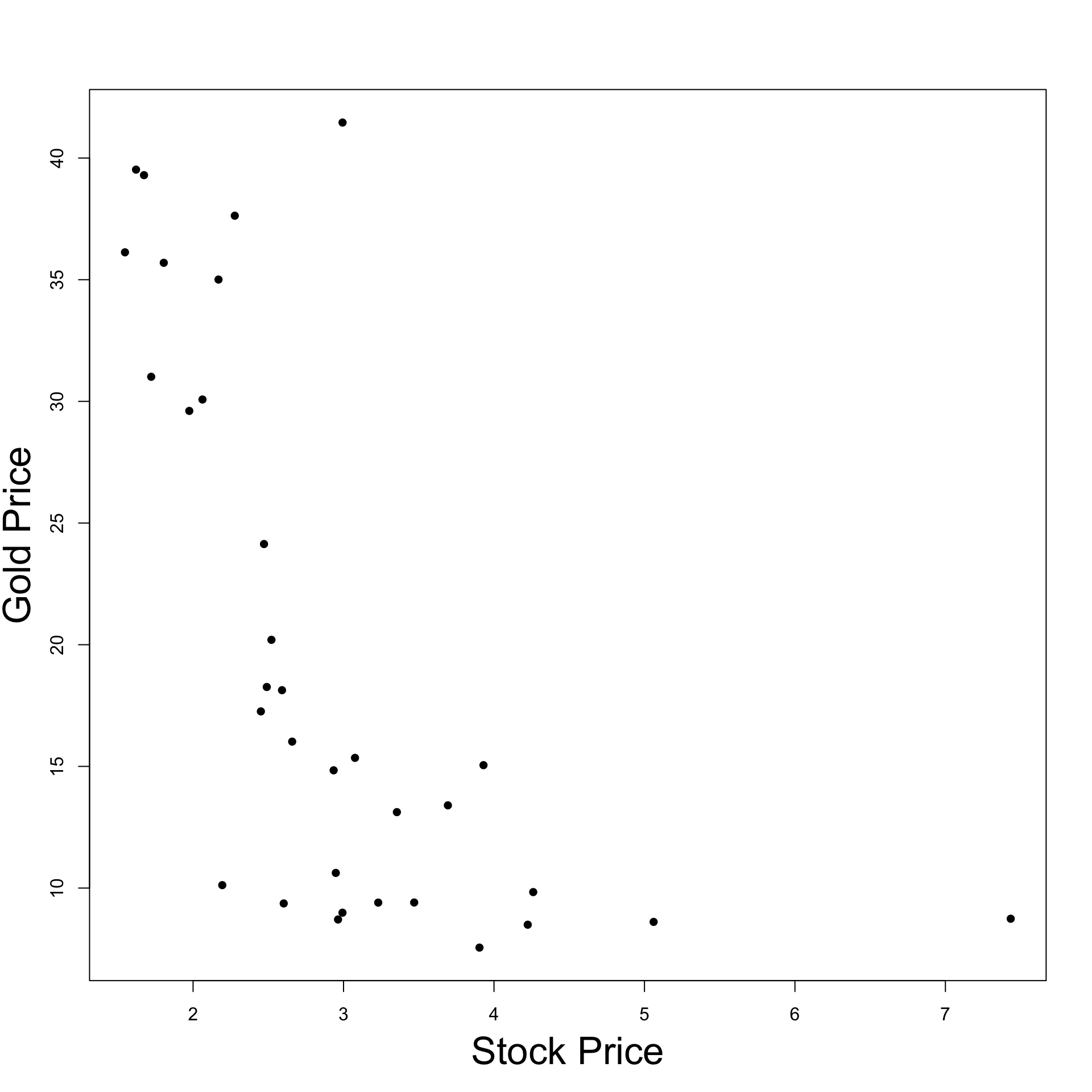

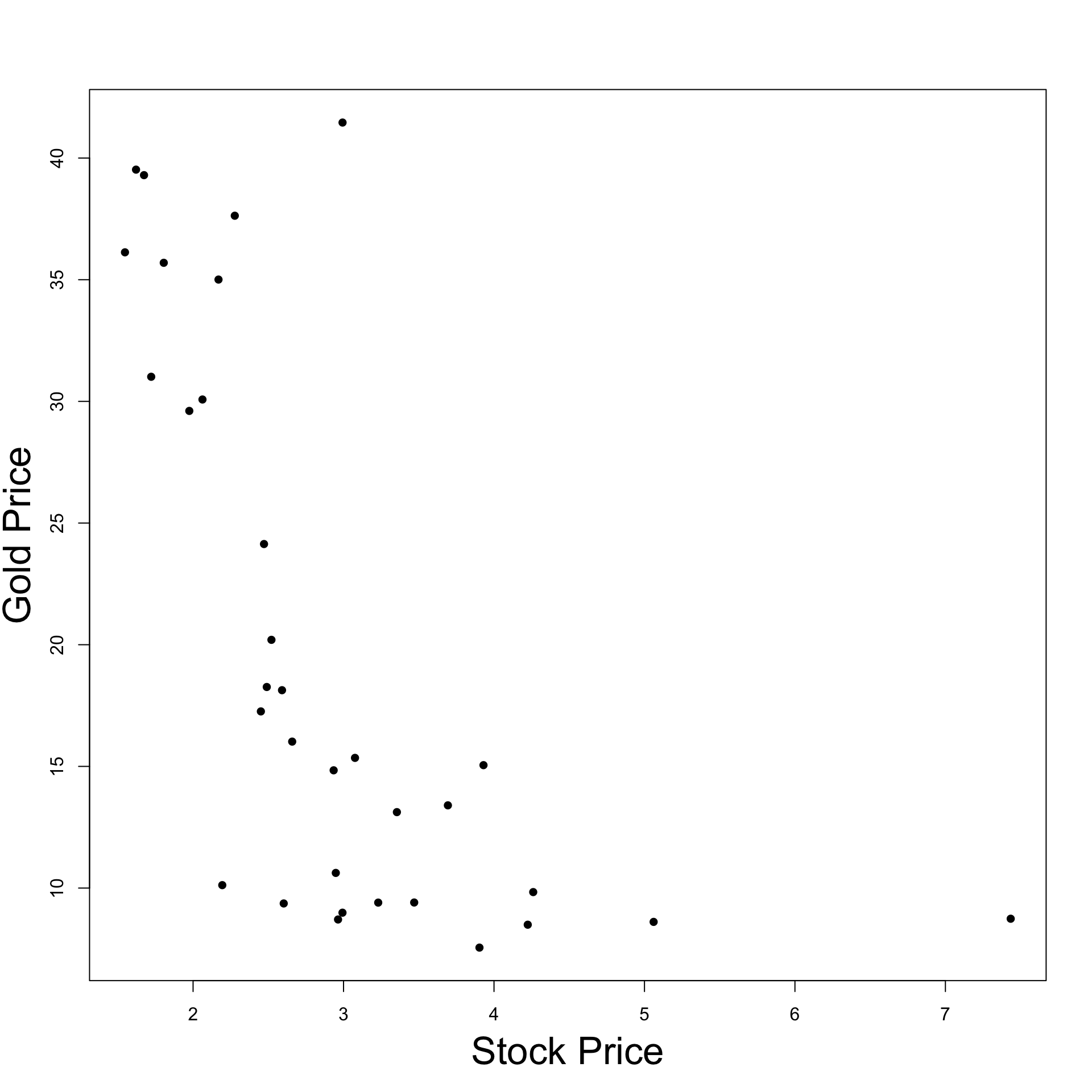

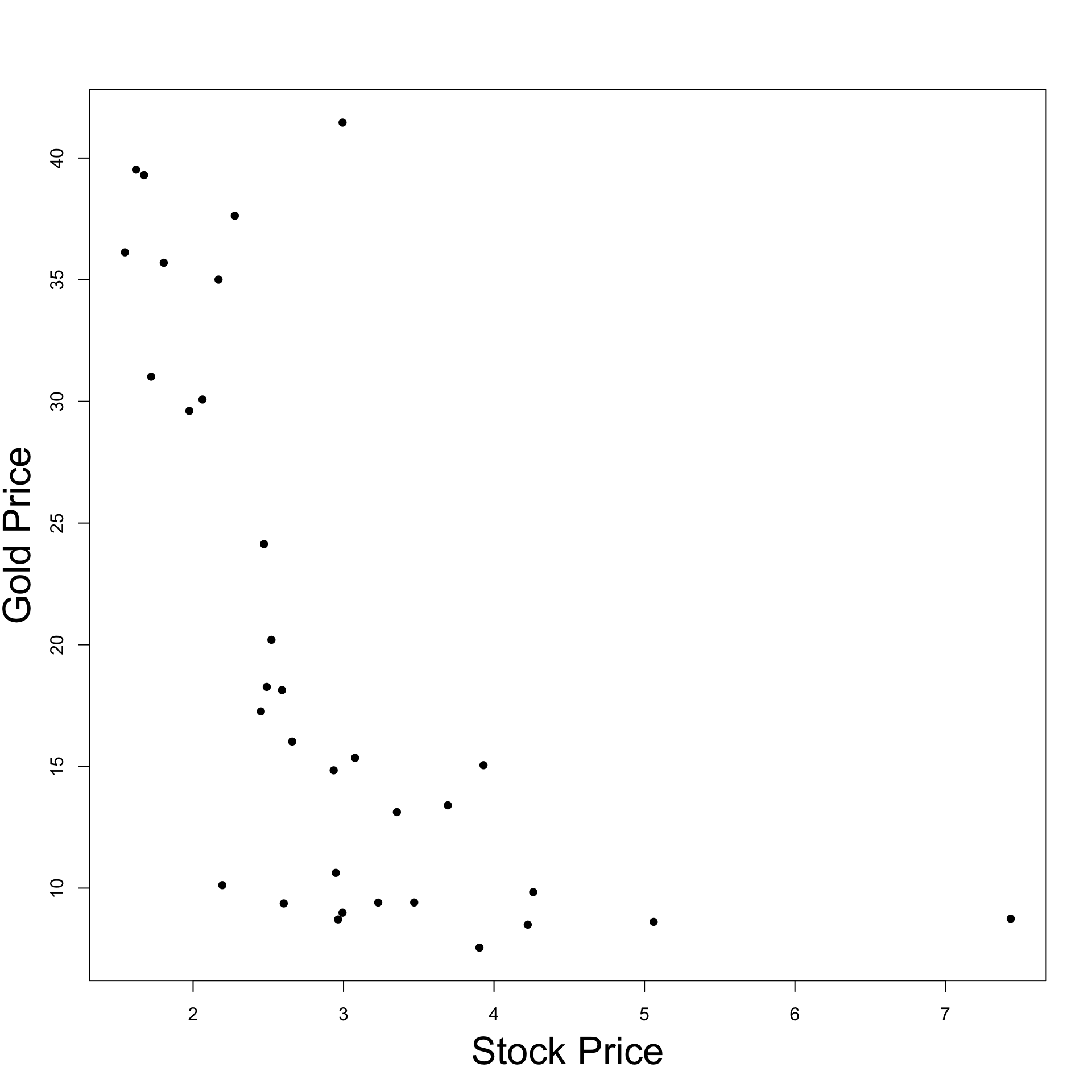

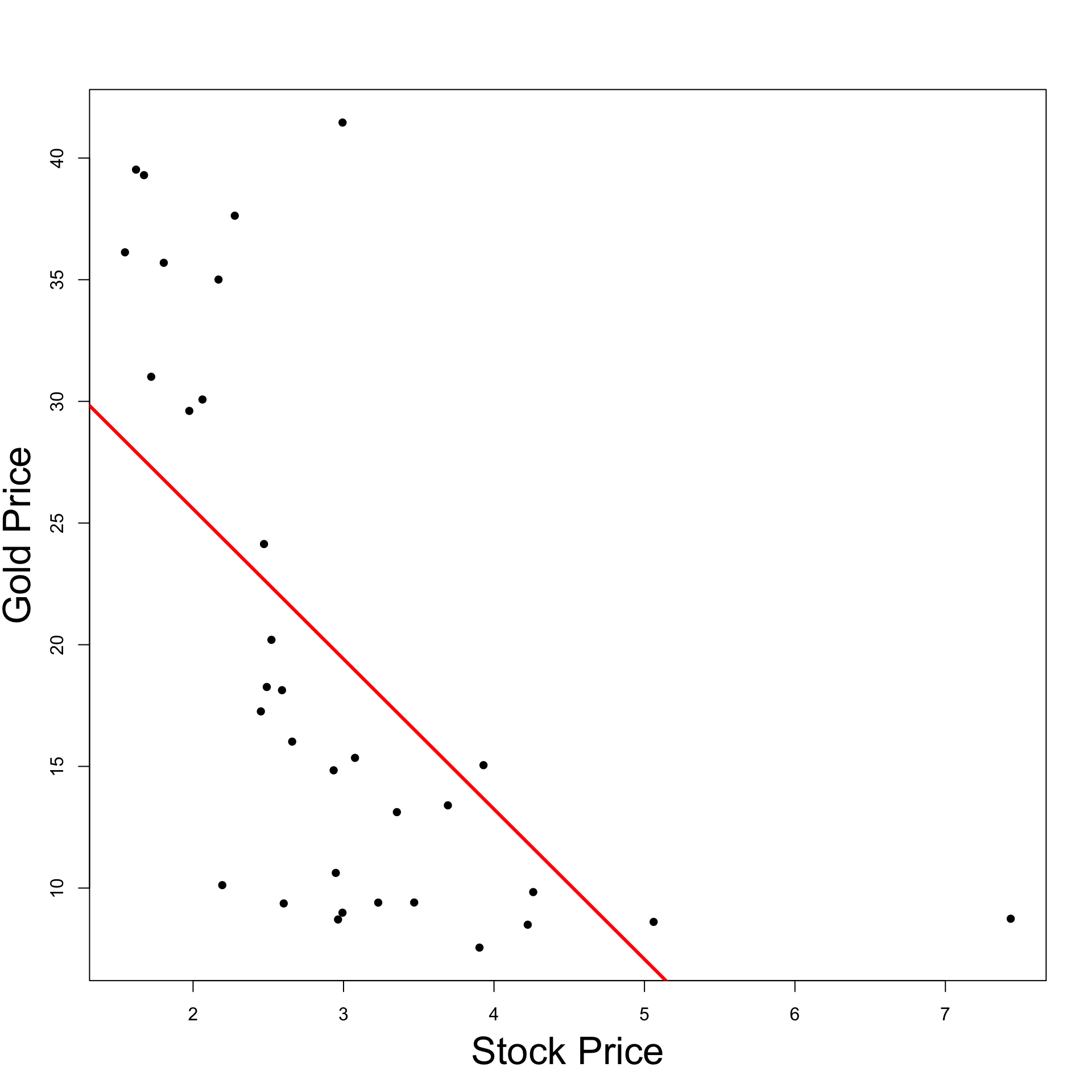

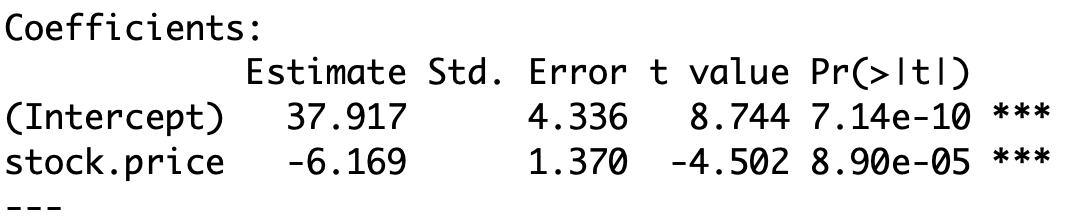

Example: Stock and Gold prices

Recall that

Y = Gold PriceX = Stock Price

We want to test if Gold Price affects Stock Price at level 0.05

Consider the linear model

Y_i = \alpha + \beta x_i + \varepsilon_i

Test the hypotheses \begin{align*}

H_0 & \colon \beta = 0 \\

H_1 & \colon \beta \neq 0

\end{align*}

Testing for \beta = 0

Recall that Stock Prices and Gold Prices are stored in R vectors

Fit the simple linear model with the following commands

\text{gold.price } = \alpha + \beta \, \times \text{ stock.price } + \text{ error}

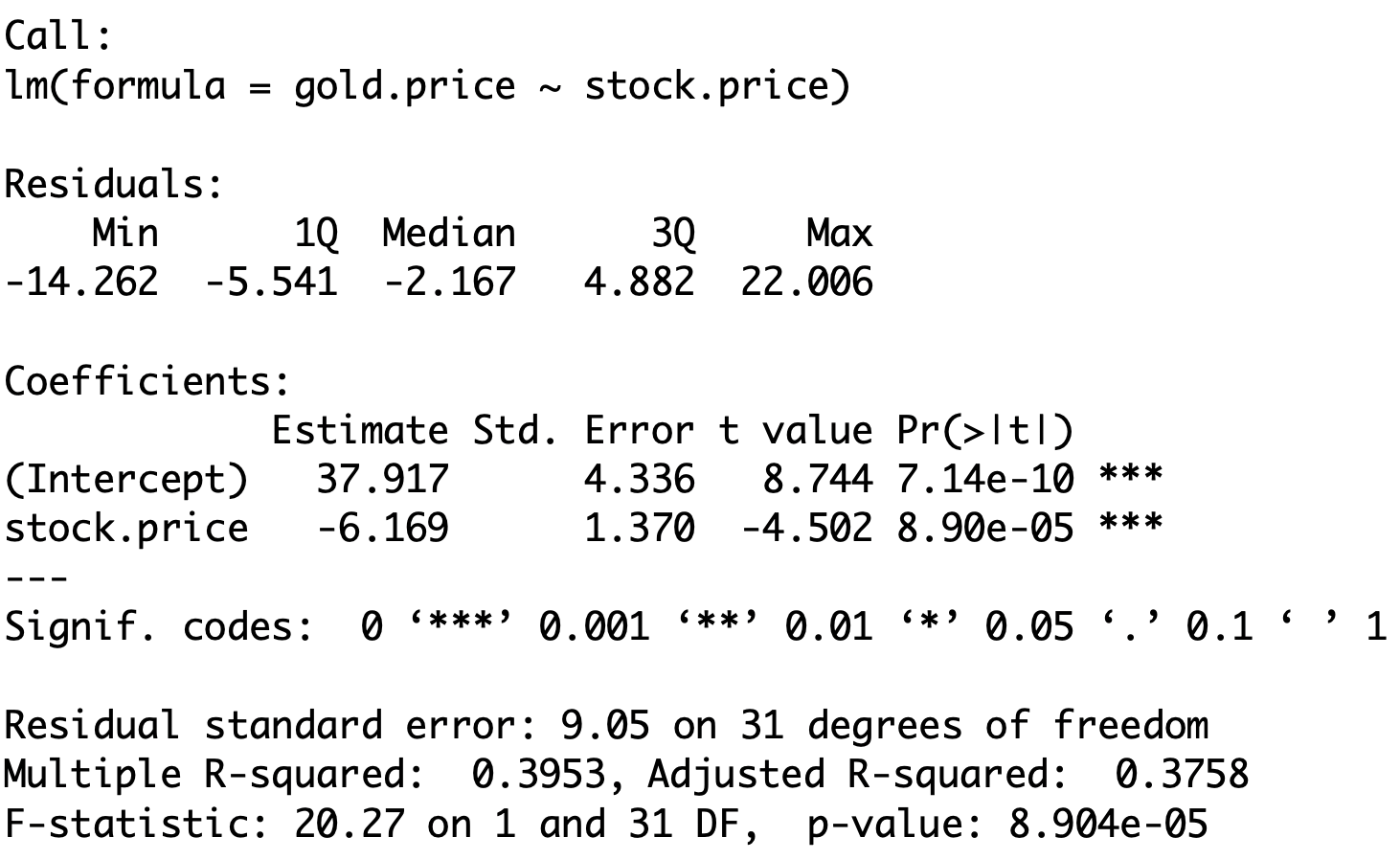

# Fit simple linear regression model <- lm (gold.price ~ stock.price)# Print result to screen summary (fit.model)

Output: \mathop{\mathrm{e.s.e.}} , t-statistic, p-value

Output: \mathop{\mathrm{e.s.e.}} , t-statistic, p-value

The 2nd row of the table has to be interpreted as follows

\texttt{Std. Error} Estimated standard error \mathop{\mathrm{e.s.e.}} for \beta

\texttt{t value} t-statistic \, t = \dfrac{\hat \beta - 0 }{\mathop{\mathrm{e.s.e.}}}

\texttt{Pr(>|t|)} p-value \, p = 2 P( t_{n-2} > |t| )

\texttt{*} , \, \texttt{**} , \, \texttt{***} , \, \texttt{.} Statistical significance – More stars is better

Output: \mathop{\mathrm{e.s.e.}} , t-statistic, p-value

The above table then gives

\hat \beta = -6.169 \,, \qquad \mathop{\mathrm{e.s.e.}}= 1.37 \, , \qquad t = - 4.502 \,, \qquad

p = 8.9 \times 10^{-5} \

The t -statistic computed by R can also be computed by hand

t = \frac{\hat \beta - 0}{ \mathop{\mathrm{e.s.e.}}}

= \frac{-6.169}{1.37} = -4.502

Output: \mathop{\mathrm{e.s.e.}} , t-statistic, p-value

n = \text{No. of data points} = 33 \,, \qquad \text{df} = n - 2 = 31

Critical value is \, t_{31}(0.025) = 2.040

|t| = 4.502 > 2.040 = t_{31}(0.025) \quad \implies \quad p < 0.05

Output: \mathop{\mathrm{e.s.e.}} , t-statistic, p-value

Interpretation: \, p is very small (hence the \, \texttt{***} \, rating)

Therefore we reject the null hypothesis H_0 and the real parameter is \beta \neq 0

Since \beta \neq 0 we have that Stock Prices affect Gold Prices

The best estimate for \beta is \hat \beta = -6.169

\hat \beta < 0 and statistically significant:\,\, As Stock Prices increase Gold Prices decrease

t-test for general regression

Consider the general linear regression model

Y_i = \beta_1 z_{i1} + \ldots + \beta_{ip} z_{ip} + \varepsilon_i \,, \qquad

\varepsilon_i \, \text{ iid } \, N(0, \sigma^2)

Z_j \,\, \text{ affects } \,\, Y \qquad \iff \qquad

\beta_j \neq 0

To see if Z_j affects Y we need to test the hypothesis

\begin{align*}

H_0 \colon & \beta_j = b_j \\

H_1 \colon & \beta_j \neq b_j

\end{align*}

Distribution of estimator \hat \beta

The estimator for the general model is

\hat \beta = (Z^T Z)^{-1} Z^T y

It can be proven that (see Section 11.5 in [2 ] )

\hat \beta_j \sim N \left( \beta_j , \xi_{jj} \sigma^2 \right)

The numbers \xi_{jj} are the diagonal entries of the p \times p matrix

(Z^T Z)^{-1} =

\left(

\begin{array}{ccc}

\xi_{11} & \ldots & \xi_{1p} \\

\ldots & \ldots & \ldots \\

\xi_{p1} & \ldots & \xi_{pp} \\

\end{array}

\right)

Construction of the t-statistic

In particular \hat \beta_j is an unbiased estimator for \beta_j

{\rm I\kern-.3em E}[ \hat \beta_j ] = \beta_j

Therefore the t-statistic for \hat \beta_j is

t = \frac{\text{Estimate } - \text{ Hypothesised Value}}{\mathop{\mathrm{e.s.e.}}}

= \frac{ \hat \beta_j - \beta_j }{ \mathop{\mathrm{e.s.e.}}}

Estimated Standard Error

{\rm Var}[\hat \beta_j] = \xi_{jj} \, \sigma^2

Hence the standard error of \hat \beta_j is the standard deviation

{\rm SD}[\hat \beta_j] = \xi_{jj}^{1/2} \, \sigma

{\rm SD} cannot be used for testing, since \sigma^2 is unknown

Estimated Standard Error

We however have an estimate for \sigma^2

\hat \sigma^2 = \frac{1}{n} \mathop{\mathrm{RSS}}= \frac1n \sum_{i=1}^n (y_i - \hat y_i)^2

{\rm I\kern-.3em E}[ \hat\sigma^2 ] = \frac{n-p}{n} \, \sigma^2

Estimated Standard Error

S^2 := \frac{n}{n-p} \, \hat\sigma^2 = \frac{\mathop{\mathrm{RSS}}}{n-p}

This way S^2 is unbiased estimator for \sigma^2

{\rm I\kern-.3em E}[S^2] = \frac{n}{n-p} \, {\rm I\kern-.3em E}[\hat\sigma^2] = \frac{n}{n-p} \, \frac{n-p}{n} \, \sigma^2 = \sigma^2

Estimated Standard Error

Recall that the standard deviation of \hat \beta is

{\rm SD}[\hat \beta] = \xi_{jj}^{1/2} \, \sigma

\mathop{\mathrm{e.s.e.}}=\xi_{jj}^{1/2} \, S

t-statistic to test \beta_j

Theorem Consider the general linear regression model

Y_i = \beta_1 z_{i1} + \ldots +\beta_p z_{ip} + \varepsilon_i

with \varepsilon_i iid N(0, \sigma^2) . Then

t = \frac{\text{Estimate } - \text{ Hypothesised Value}}{\mathop{\mathrm{e.s.e.}}} = \frac{ \hat \beta_j - \beta_j }{ \xi_{jj}^{1/2} \, S}

\, \sim \,

t_{n-p}

Proof: See section 11.5 in [2 ]

Summary: t-test for \beta_j

Goal : Estimate the coefficient \beta_j for the general linear model

Y_i = \beta_1 z_{i1} + \ldots + \beta_p z_{ip} + \varepsilon_i \,, \qquad \varepsilon_i \, \text{ iid } \, N(0,\sigma^2)

Hypotheses : If b_j is guess for \beta_j the hypotheses are

\begin{align*}

H_0 & \colon \beta_j = b_j \\

H_1 & \colon \beta_j \neq b_j

\end{align*}

Summary: t-test for \beta_j

t = \frac{\hat \beta_j - b_j }{ \mathop{\mathrm{e.s.e.}}} \, \sim \, t_{n-p} \,, \qquad \quad

\mathop{\mathrm{e.s.e.}}= \xi_{jj}^{1/2} \, S

In the above \xi_{jj} are diagonal entries of (Z^TZ)^{-1} and

\hat \beta = (Z^TZ)^{-1} Z^T y \,, \qquad \quad S^2 := \frac{\mathop{\mathrm{RSS}}}{n-p}

p = 2P (t_{n-p} > |t|)

t-test in R: Fit general regression with lm

If b_j = 0 and a two-sided t-test is required

t-statistic is in j -th variable row under \,\, \texttt{t value}

p-value is in j -th variable row under \,\, \texttt{Pr(>|t|)}

If b_j \neq 0 or one-sided t-test is required

Compute t-statistic by hand

t = \frac{\hat \beta_j - b_j}{\mathop{\mathrm{e.s.e.}}}

\,\, \hat \beta_j is in j -th variable row under \,\, \texttt{Estimate} \,\, \mathop{\mathrm{e.s.e.}} for \hat \beta_j is in j -th variable row under \,\, \texttt{Std. Error} Compute p-value by hand with \,\, \texttt{pt(t, df)}

Example: \mathop{\mathrm{e.s.e.}} for simple linear regression

Consider the simple regression model

Y_i = \alpha + \beta x_i + \varepsilon_i

Z = \left(

\begin{array}{cc}

1 & x_1 \\

\ldots & \ldots \\

1 & x_n \\

\end{array}

\right)

Example: \mathop{\mathrm{e.s.e.}} for simple linear regression

We have seen in Lecture 9 that

(Z^T Z)^{-1} =

\frac{1}{n S_{xx} }

\left(

\begin{array}{cc}

\sum_{i=1}^n x^2_i & -n \overline{x}\\

-n\overline{x} & n

\end{array}

\right)

Hence the \mathop{\mathrm{e.s.e.}} for \hat \alpha and \hat \beta are

\begin{align*}

\mathop{\mathrm{e.s.e.}}(\hat \alpha) & = \xi_{11}^{1/2} \, S^2 = \sqrt{ \frac{ \sum_{i=1}^n x_i^2 }{ n S_{xx} } } \, S^2 \\[7pt]

\mathop{\mathrm{e.s.e.}}(\hat \beta) & = \xi_{22}^{1/2} \, S^2 = \frac{ S^2 }{ \sqrt{ S_{xx} } }

\end{align*}

Note: \, \mathop{\mathrm{e.s.e.}}(\hat\beta) coincides with the \mathop{\mathrm{e.s.e.}} in Slide 50

Part 4:

F-test for overall significance

Want to test the overall significance of the model

Y_i = \beta_1 + \beta_2 x_{i2} + \ldots + \beta_p x_{ip} + \varepsilon_i

This means answering the question:

\text{ Does at least one } X_i \text{ affect } Y \text{ ?}

How to do this?

Could perform a sequence of t-tests on the \beta_j

For statistical reasons this is not really desirable

To assess overall significance we can perform F-test

F-test for overall significance

The F-test for overall significance has 3 steps:

Define a larger full model (with more parameters)

Define a smaller nested reduced model (with fewer parameters)

Use an F-statistic to decide between larger or smaller model

Overall significance for multiple regression

Model 1 is the smaller reduced model

Model 2 is the larger full model

\begin{align*}

\textbf{Model 1:} & \quad Y_i = \beta_1 + \varepsilon_i \\[15pt]

\textbf{Model 2:} & \quad Y_i = \beta_1 + \beta_2 x_{i2} + \ldots + \beta_p x_{ip} + \varepsilon_i

\end{align*}

Choosing the smaller Model 1 is equivalent to accepting H_0

\begin{align*}

H_0 & \colon \, \beta_2 = \beta_3 = \ldots = \beta_p = 0 \\

H_1 & \colon \text{ At least one of the } \beta_i \text{ is non-zero}

\end{align*}

Overall significance for simple regression

Model 1 is the smaller reduced model

Model 2 is the larger full model

\begin{align*}

\textbf{Model 1:} & \quad Y_i = \alpha + \varepsilon_i \\[15pt]

\textbf{Model 2:} & \quad Y_i = \alpha + \beta x_i + \varepsilon_i

\end{align*}

Choosing the smaller Model 1 is equivalent to accepting H_0

\begin{align*}

H_0 & \colon \beta = 0 \\

H_1 & \colon \beta \neq 0

\end{align*}

Construction of F-statistic

Consider the full model with p parameters

\textbf{Model 2:} \quad Y_i = \beta_1 + \beta_2 x_{i2} + \ldots + \beta_p x_{ip} + \varepsilon_i

Predictions for the full model are

\hat y_i := \beta_1 + \beta_2 x_{i2} + \ldots + \beta_p x_{ip}

Define the residual sum of squares for the full model

\mathop{\mathrm{RSS}}(p) := \sum_{i=1}^n (y_i - \hat y_i)^2

Construction of F-statistic

Consider now the reduced model

\textbf{Model 1:} \quad Y_i = \beta_1 + \varepsilon_i

Predictions of the reduced model are constant

\hat y_i = \beta_1

Define the residual sum of squares for the full model

\mathop{\mathrm{RSS}}(1) := \sum_{i=1}^n (y_i - \beta_1)^2

Construction of F-statistic

Suppose the parameters of the full model

\beta_2, \ldots, \beta_p

are not important

In this case the predictions of full and reduced model will be similar

Therefore the \mathop{\mathrm{RSS}} for the 2 models are similar

\mathop{\mathrm{RSS}}(1) \, \approx \, \mathop{\mathrm{RSS}}(p)

Construction of F-statistic

Recall that \mathop{\mathrm{RSS}} is defined via minimization

\mathop{\mathrm{RSS}}(k) := \min_{\beta_1 , \ldots , \beta_k} \ \sum_{i=1}^n ( y_i - \hat y_i)^2 \,, \qquad

\hat y_i := \beta_1 + \beta_2 x_{i2} + \ldots + \beta_k x_{ik}

Therefore \mathop{\mathrm{RSS}} cannot increase if we add parameters to the model

\mathop{\mathrm{RSS}}(1) \geq \mathop{\mathrm{RSS}}(p)

To measure how influential the parameters \beta_2, \ldots, \beta_p are, we study

\frac{\mathop{\mathrm{RSS}}(1) - \mathop{\mathrm{RSS}}(p)}{\mathop{\mathrm{RSS}}(p)}

Construction of F-statistic

\frac{\mathop{\mathrm{RSS}}(1) - \mathop{\mathrm{RSS}}(p)}{\mathop{\mathrm{RSS}}(p)}

To this end, note that the degrees of freedom of reduced model are

\mathop{\mathrm{df}}(1) = n - 1

The degrees of freedom of the full model are

\mathop{\mathrm{df}}(p) = n - p

F-statistic for overall significance

Definition The

F-statistic for overall significance is

\begin{align*}

F & := \frac{\mathop{\mathrm{RSS}}(1) - \mathop{\mathrm{RSS}}(p)}{ \mathop{\mathrm{df}}(1) - \mathop{\mathrm{df}}(p) } \bigg/

\frac{\mathop{\mathrm{RSS}}(p)}{\mathop{\mathrm{df}}(p)} \\[15pt]

& = \frac{\mathop{\mathrm{RSS}}(1) - \mathop{\mathrm{RSS}}(p)}{ p - 1 } \bigg/

\frac{\mathop{\mathrm{RSS}}(p)}{n - p}

\end{align*}

Theorem: The F-statistic for overall significance has F-distribution

F \, \sim \, F_{p-1,n-p}

Rewriting the F-statistic

Proposition The F-statistic can be rewritten as

\begin{align*}

F & = \frac{\mathop{\mathrm{RSS}}(1) - \mathop{\mathrm{RSS}}(p)}{ p - 1 } \bigg/

\frac{\mathop{\mathrm{RSS}}(p)}{n - p} \\[15pt]

& = \frac{R^2}{1 - R^2} \, \cdot \, \frac{n - p}{p - 1}

\end{align*}

Proof of Proposition

Notice that \mathop{\mathrm{TSS}} does not depend on p since

\mathop{\mathrm{TSS}}= \sum_{i=1}^n (y_i - \overline{y})^2

Recall the definition of R^2

R^2 = 1 - \frac{\mathop{\mathrm{RSS}}(p)}{\mathop{\mathrm{TSS}}}

\mathop{\mathrm{RSS}}(p) = (1 - R^2) \mathop{\mathrm{TSS}}

Proof of Proposition

By definition we have that

\mathop{\mathrm{RSS}}(1) = \min_{\beta_1} \ \sum_{i=1}^n (y_i - \beta_1)^2

Exercise: Check that the unique solution to the above problem is

\beta_1 = \overline{y}

\mathop{\mathrm{RSS}}(1) = \sum_{i=1}^n (y_i - \overline{y})^2 = \mathop{\mathrm{TSS}}

Proof of Proposition

We just obtained the two identities

\mathop{\mathrm{RSS}}(p) = (1 - R^2) \mathop{\mathrm{TSS}}\,, \qquad \quad \mathop{\mathrm{RSS}}(1) = \mathop{\mathrm{TSS}}

From the above we conclude the proof

\begin{align*}

F & = \frac{\mathop{\mathrm{RSS}}(1) - \mathop{\mathrm{RSS}}(p)}{ p - 1 } \bigg/

\frac{\mathop{\mathrm{RSS}}(p)}{n - p} \\[15pt]

& = \frac{\mathop{\mathrm{TSS}}- (1 - R^2) \mathop{\mathrm{TSS}}}{ p - 1 } \bigg/

\frac{(1 - R^2) \mathop{\mathrm{TSS}}}{n - p}\\[15pt]

& = \frac{R^2}{1 - R^2} \, \cdot \, \frac{n - p}{p - 1}

\end{align*}

F-statistic for simple regression

Proposition

The F -statistic for overall significance in simple regression is

F = t^2 \,, \qquad \quad t = \frac{\hat \beta}{ S / \sqrt{S_{xx}}}

where t is the t-statistic for \hat \beta .

In particular the p-values for t-test and F-test coincide

p = P( t_{n-2} > |t| ) = P( F_{1,n-2} > F )

Proof: Will be left as an exercise

Summary: F-test for overall significance

Goal: Test the overall significance of the model

Y_i = \beta_1 + \beta_2 x_{i2} + \ldots + \beta_p x_{ip} + \varepsilon_i

This means answering the question:

\text{ Does at least one } X_i \text{ affect } Y \text{ ?}

Hypotheses: The above question is equivalent to testing

\begin{align*}

H_0 & \colon \, \beta_2 = \beta_3 = \ldots = \beta_p = 0 \\

H_1 & \colon \text{ At least one of the } \beta_i \text{ is non-zero}

\end{align*}

Summary: F-test for overall significance

\begin{align*}

F & = \frac{\mathop{\mathrm{RSS}}(1) - \mathop{\mathrm{RSS}}(p)}{ p - 1 } \bigg/

\frac{\mathop{\mathrm{RSS}}(p)}{n - p} \\[15pt]

& = \frac{R^2}{1 - R^2} \, \cdot \, \frac{n - p}{p - 1}

\end{align*}

F \, \sim \, F_{p-1,n-p}

Summary: F-test for overall significance

p = P ( F_{p-1,n-2} > F)

F-test in R:

Fit the multiple regression model with lm

F-statistic is listed in the summary

p-value is listed in the summary

Example: Stock and Gold prices

Recall that

Y = Gold PriceX = Stock Price We want to test the overall significance of the model

Y_i = \alpha + \beta x_i + \varepsilon_i

To this end, perform F-test for the hypotheses

\begin{align*}

H_0 & \colon \beta = 0 \\

H_1 & \colon \beta \neq 0

\end{align*}

F-test for overall significance

Recall that Stock Prices and Gold Prices are stored in R vectors

Fit the simple linear model with the following commands

\text{gold.price } = \alpha + \beta \, \times \text{ stock.price } + \text{ error}

# Fit simple linear regression model <- lm (gold.price ~ stock.price)# Print result to screen summary (fit.model)

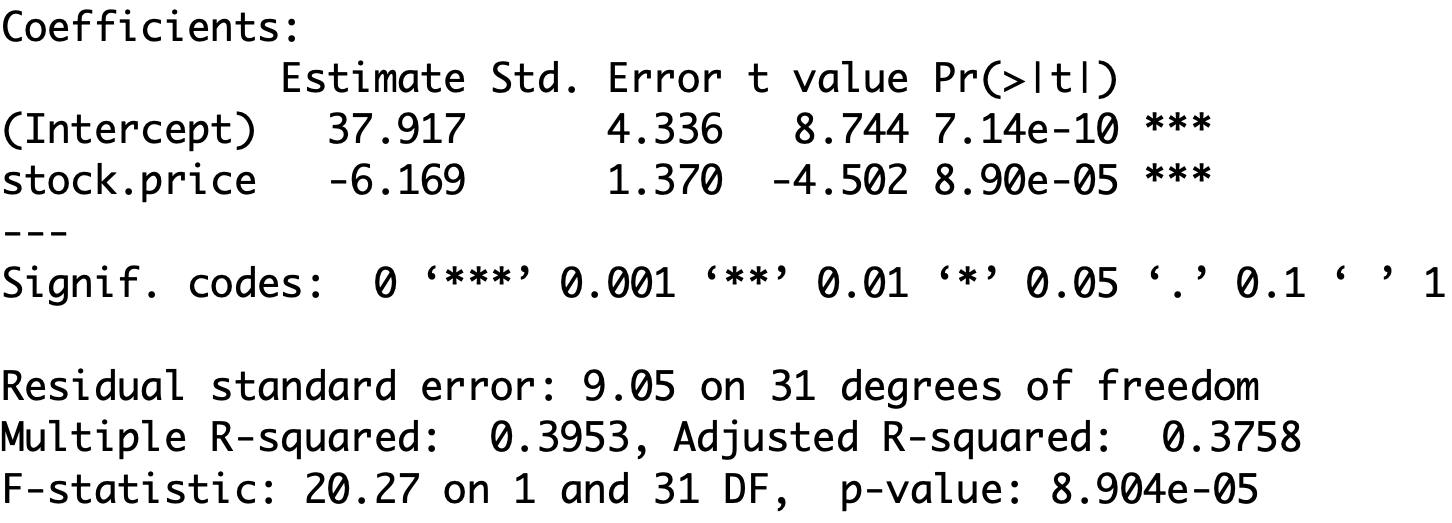

Output: F-statistic and p-value

F-statistic is F = 20.27

Degrees of freedom are 1 and 31 , meaning that F \, \sim \, F_{1,31}

The p-value is

p = P( F_{1,31} > F ) = 8.904 \times 10^{-5}

Conclusion: Strong evidence (p=0.000 ) that Stock Price affects Gold Price

Output: F-statistic and p-value

We can also compute F-statistic by hand

F = \frac{ R^2 }{ 1 - R^2 } \, \cdot \, \frac{n-p}{p-1} = \frac{0.395325}{0.604675} \, \cdot \, \frac{31}{1} = 20.267

Output: F-statistic and p-value

The p-value cannot be computed by hand

However we can find critical values close to F_{1,31} (0.05) on Tables

F_{1, 30} (0.05) = 4.17 \,, \qquad \quad F_{1, 40} (0.05) = 4.08

Output: F-statistic and p-value

We can approximate F_{1,31} (0.05) by averaging the found values

F_{1,31}(0.05) \, \approx \, \frac{F_{1, 30} (0.05) + F_{1, 40} (0.05)}{2} = 4.125

F = 20.267 > 4.125 = F_{1,31}(0.05) \quad \implies \quad p < 0.05

Testing regression parameters

Summary: We have seen

t-test

Test the significance of individual parameters \begin{align*}

H_0 & \colon \, \beta_j = 0 \\

H_1 & \colon \, \beta_j \neq 0

\end{align*}

Testing regression parameters

F-test

Test the overall significance of the model

This is done by comparing two nested regression models \begin{align*}

\textbf{Model 1:} & \qquad Y_ i= \beta_1 + \varepsilon_i \\[10pt]

\textbf{Model 2:} & \qquad Y_ i= \beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_p x_{p, i} + \varepsilon_i

\end{align*}

The comparison is achieved with F-test for \begin{align*}

H_0 & \colon \, \beta_2 = \beta_3 = \ldots = \beta_p = 0 \\

H_1 & \colon \text{ At least one of the } \beta_i \text{ is non-zero}

\end{align*}

Choosing Model 1 is equivalent to accepting H_0

More general nested models

Consider the more general nested models

\begin{align*}

\textbf{Model 1:} & \quad Y_ i =\beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \varepsilon_i \\[10pt]

\textbf{Model 2:} & \quad Y_ i= \beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \beta_{k + 1} x_{k + 1, i} +

\ldots + \beta_{p} x_{p, i} + \varepsilon_i

\end{align*}

\beta_{k + 1} = \beta_{k + 2} = \ldots = \beta_p = 0

Question: How do we decide which model is better?

Model selection

Consider the more general nested models

\begin{align*}

\textbf{Model 1:} & \quad Y_ i =\beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \varepsilon_i \\[10pt]

\textbf{Model 2:} & \quad Y_ i= \beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \beta_{k + 1} x_{k + 1, i} +

\ldots + \beta_{p} x_{p, i} + \varepsilon_i

\end{align*}

Define the predictions for the two models

\begin{align*}

\hat y_i^1 & := \beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} \\[10pt]

\hat y_i^2 & := \beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \beta_{k + 1} x_{k + 1, i} +

\ldots + \beta_{p} x_{p, i}

\end{align*}

Model selection

Consider the more general nested models

\begin{align*}

\textbf{Model 1:} & \quad Y_ i =\beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \varepsilon_i \\[10pt]

\textbf{Model 2:} & \quad Y_ i= \beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \beta_{k + 1} x_{k + 1, i} +

\ldots + \beta_{p} x_{p, i} + \varepsilon_i

\end{align*}

\mathop{\mathrm{RSS}} measures variation between data and prediction

\begin{align*}

\textbf{Model 1:} & \quad \mathop{\mathrm{RSS}}_1 := \mathop{\mathrm{RSS}}(k) = \sum_{i=1}^n (y_i - \hat y_i^1)^2 \\[10pt]

\textbf{Model 2:} & \quad \mathop{\mathrm{RSS}}_2 := \mathop{\mathrm{RSS}}(p) = \sum_{i=1}^n (y_i - \hat y_i^2)^2

\end{align*}

Construction of F-statistic

Goal: Use \mathop{\mathrm{RSS}} to construct statistic to compare the 2 models

Suppose the extra parameters of Model 2

\beta_{k+1}, \, \beta_{k+2} , \, \ldots , \, \beta_p

are not important

Hence the predictions of the 2 models will be similar

\hat y_i^1 \, \approx \, \hat y_i^2

Therefore the \mathop{\mathrm{RSS}} for the 2 models are similar

\mathop{\mathrm{RSS}}_1 \, \approx \, \mathop{\mathrm{RSS}}_2

Construction of F-statistic

Recall that \mathop{\mathrm{RSS}} cannot increase if we increase parameters

k < p \quad \implies \quad \mathop{\mathrm{RSS}}(k) \geq \mathop{\mathrm{RSS}}(p)

To measure influence of extra parameters

\beta_{k+1}, \, \beta_{k+2} , \, \ldots , \, \beta_p

we consider the ratio

\frac{ \mathop{\mathrm{RSS}}_1 - \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{RSS}}_2 } = \frac{ \mathop{\mathrm{RSS}}(k) - \mathop{\mathrm{RSS}}(p) }{ \mathop{\mathrm{RSS}}(p) }

Construction of F-statistic

\frac{ \mathop{\mathrm{RSS}}_1 - \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{RSS}}_2 }

Note that the degrees of freedom are

Model 1:

k \text{ parameters } \quad \implies \quad \mathop{\mathrm{df}}_1 = n - k

Model 2:

p \text{ parameters } \quad \implies \quad \mathop{\mathrm{df}}_2 = n - p

F-statistic for model selection

Definition The F-statistic for model selection is

\begin{align*}

F & = \frac{ \mathop{\mathrm{RSS}}_1 - \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{df}}_1 - \mathop{\mathrm{df}}_2 } \bigg/

\frac{ \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{df}}_2 } \\[20pt]

& = \frac{ \mathop{\mathrm{RSS}}(k) - \mathop{\mathrm{RSS}}(p) }{ p - k } \bigg/

\frac{ \mathop{\mathrm{RSS}}(p) }{ n - p }

\end{align*}

Theorem: The F-statistic for model selection has F-distribution

F \, \sim \, F_{\mathop{\mathrm{df}}_1 - \mathop{\mathrm{df}}_2 , \, \mathop{\mathrm{df}}_2} = F_{p - k, \, n - p}

Rewriting the F-statistic

Recall the formulas for sums of squares

\mathop{\mathrm{TSS}}= \mathop{\mathrm{ESS}}(p) + \mathop{\mathrm{RSS}}(p) \,, \qquad \quad

\mathop{\mathrm{TSS}}= \mathop{\mathrm{ESS}}(k) + \mathop{\mathrm{RSS}}(k)

R_1^2 := R^2 (k) := \frac{ \mathop{\mathrm{ESS}}(k) }{ \mathop{\mathrm{TSS}}}

\, , \qquad \quad

R_2^2 := R^2 (p) := \frac{ \mathop{\mathrm{ESS}}(p) }{ \mathop{\mathrm{TSS}}}

Rewriting the F-statistic

\begin{align*}

\mathop{\mathrm{RSS}}(k) - \mathop{\mathrm{RSS}}(p) & = \mathop{\mathrm{ESS}}(p) - \mathop{\mathrm{ESS}}(k) \\[10pt]

& = \mathop{\mathrm{TSS}}( R^2(p) - R^2(k) ) \\[10pt]

& = \mathop{\mathrm{TSS}}( R^2_2 - R^2_1 ) \\[20pt]

\mathop{\mathrm{RSS}}(p) & = \mathop{\mathrm{TSS}}- \mathop{\mathrm{ESS}}(p) \\[10pt]

& = \mathop{\mathrm{TSS}}- \mathop{\mathrm{TSS}}\, \cdot \, R^2 (p) \\[10pt]

& = \mathop{\mathrm{TSS}}(1 - R^2(p)) \\[10pt]

& = \mathop{\mathrm{TSS}}(1 - R_2^2)

\end{align*}

Rewriting the F-statistic

Therefore the F-statistic can be rewritten as

\begin{align*}

F & = \frac{ \mathop{\mathrm{RSS}}_1 - \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{df}}_1 - \mathop{\mathrm{df}}_2 } \bigg/

\frac{ \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{df}}_2 } \\[20pt]

& = \frac{ \mathop{\mathrm{TSS}}(R^2_2 - R^2_1) }{\mathop{\mathrm{TSS}}(1 - R^2_2 )} \, \cdot \, \frac{n-p}{p-k} \\[20pt]

& = \frac{ R^2_2 - R^2_1 }{1 - R^2_2} \, \cdot \, \frac{n-p}{p-k}

\end{align*}

F-test for overall significance revisited

The F-test for overall significance allows to select between models \begin{align*}

\textbf{Model 1:} & \qquad Y_ i= \beta_1 + \varepsilon_i \\[10pt]

\textbf{Model 2:} & \qquad Y_ i= \beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_p x_{p, i} + \varepsilon_i

\end{align*}

Model 1 has k = 1 parameters

F-statistic for model selection coincides with F-statistic for overall significance

F = \frac{ \mathop{\mathrm{RSS}}(1) - \mathop{\mathrm{RSS}}(p) }{ p - 1 } \bigg/

\frac{ \mathop{\mathrm{RSS}}(p) }{ n - p }

Summary: F-test for model selection

Goal: Choose one of the nested models

\begin{align*}

\textbf{Model 1:} & \quad Y_ i =\beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \varepsilon_i \\[10pt]

\textbf{Model 2:} & \quad Y_ i= \beta_1 + \beta_2 x_{2, i}+ \ldots + \beta_{k} x_{k, i} + \beta_{k + 1} x_{k + 1, i} +

\ldots + \beta_{p} x_{p, i} + \varepsilon_i

\end{align*}

Hypotheses: Choosing a model is equivalent to testing

\begin{align*}

H_0 \colon & \, \beta_{k+1} = \beta_{k+2} = \ldots = \beta_p \\[5pt]

H_1 \colon & \, \text{ At least one among } \beta_{k+1}, \ldots, \beta_p \text{ is non-zero}

\end{align*}

H_0 is in favor of Model 1H_1 is in favor of Model 2

Summary: F-test for model selection

\begin{align*}

F & = \frac{ \mathop{\mathrm{RSS}}_1 - \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{df}}_1 - \mathop{\mathrm{df}}_2 } \bigg/

\frac{ \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{df}}_2 } \\[20pt]

& = \frac{ R^2_2 - R^2_1 }{1 - R^2_2 } \, \cdot \, \frac{n-p}{p-k}

\end{align*}

F \, \sim \, F_{ \mathop{\mathrm{df}}_1 - \mathop{\mathrm{df}}_2 , \, \mathop{\mathrm{df}}_2 } = F_{p-k, \, n-p}

Summary: F-test for model selection

p = P(F_{p-k,n-p} > F)

F-test for model selection in R:

Fit the two models with \,\texttt{lm}

Use the command \, \texttt{anova} \qquad\quad (more on this later)

Alternative:

Find R^2_1 and R^2_2 in summary

Compute F-statistic and p-value

Part 7:

Examples of model selection

We illustrate F-test for Model Selection with 3 examples:

Joint significance in Multiple linear Regression

Polynomial regression 1

Polynomial regression 2

Example 1: Multiple linear regression

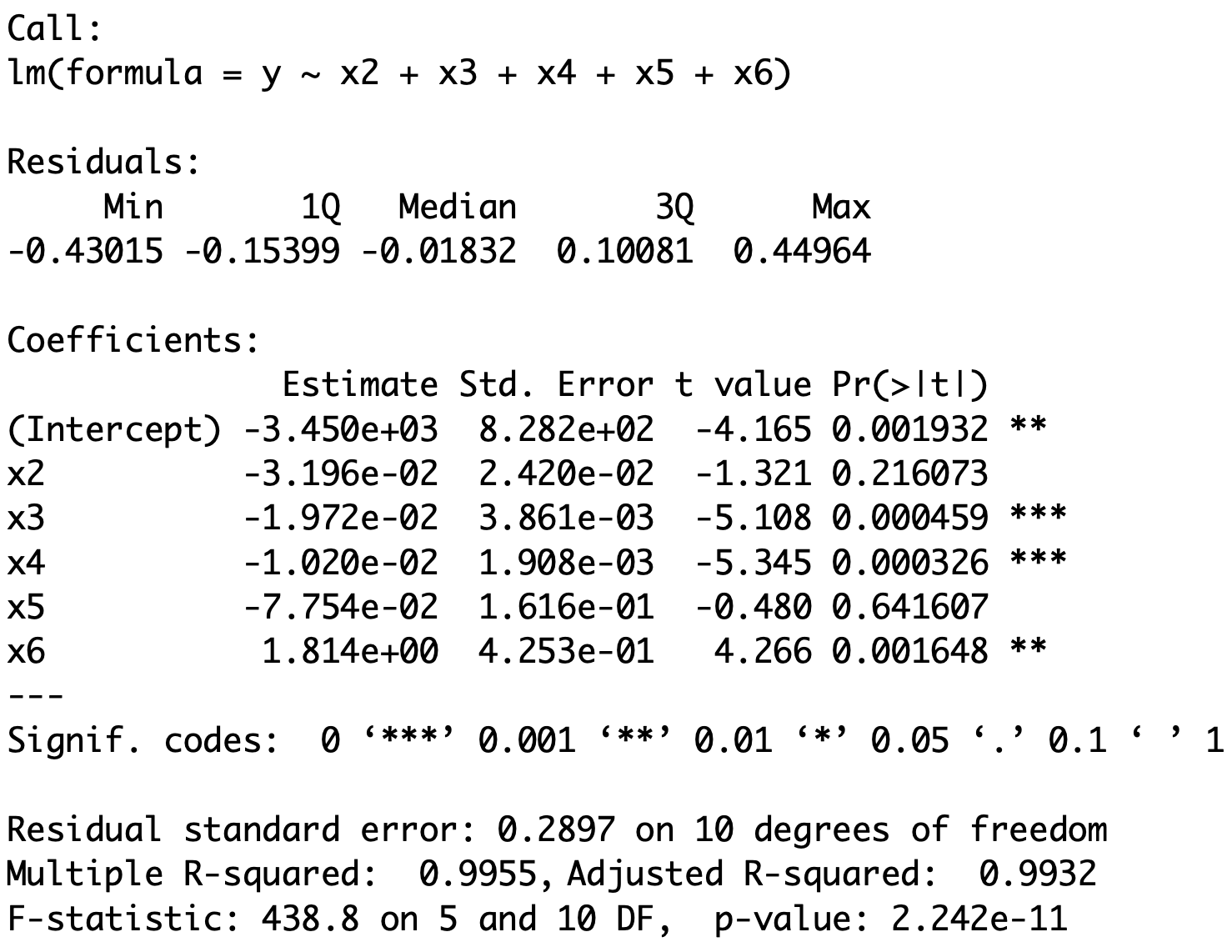

Consider again the Longley dataset

GNP Unemployed Armed.Forces Population Year Employed

1 234.289 235.6 159.0 107.608 1947 60.323

2 259.426 232.5 145.6 108.632 1948 61.122

3 258.054 368.2 161.6 109.773 1949 60.171

Goal: Explain the number of Employed people Y in the US in terms of

X_2 GNP Gross National ProductX_3 number of Unemployed X_4 number of people in the Armed Forces X_5 non-institutionalised Population \geq age 14 (not in care of insitutions)X_6 Years from 1947 to 1962

Example 1: Multiple linear regression

Previously: Using t-test for parameters significance we showed that

X_2 and X_5 do not affect Y X_3 and X_4 negatively affect Y X_6 positively affects Y

Question: Since X_2 and X_5 do not affect Y , can we exclude them from the model?

Two competing models

We therefore want to select between the models:

Model 1: The reduced model without X_2 and X_5

Y = \beta_1 + \beta_3 X_3 + \beta_4 X_4 +

\beta_6 X_6 + \varepsilon

Y = \beta_1 + \beta_2 X_2 + \beta_3 X_3 + \beta_4 X_4 +

\beta_5 X_5 + \beta_6 X_6 + \varepsilon

R commands for reading in the data

We read the data in the same way we did earlier

Longley dataset available here longley.txt

Download the file and place it in current working directory

# Read data file <- read.table (file = "longley.txt" ,header = TRUE )# Store columns in vectors <- longley[ , 1 ]<- longley[ , 2 ]<- longley[ , 3 ]<- longley[ , 4 ]<- longley[ , 5 ]<- longley[ , 6 ]

R commands for fitting multiple regression

Fit the two multiple regression models

\begin{align*}

\textbf{Model 1:} & \quad Y = \beta_1 + \beta_3 X_3 + \beta_4 X_4 +

\beta_6 X_6 + \varepsilon\\[10pt]

\textbf{Model 2:} & \quad Y = \beta_1 + \beta_2 X_2 + \beta_3 X_3 + \beta_4 X_4 +

\beta_5 X_5 + \beta_6 X_6 + \varepsilon

\end{align*}

# Fit Model 1 and Model 2 .1 <- lm (y ~ x3 + x4 + x6).2 <- lm (y ~ x2 + x3 + x4 + x5 + x6)

F-test for model selection is done using the command \, \texttt{anova}

# F-test for model selection anova (model.1 , model.2 , test = "F" )

Anova output

Analysis of Variance Table

Model 1: y ~ x3 + x4 + x6

Model 2: y ~ x2 + x3 + x4 + x5 + x6

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 1.32336

2 10 0.83935 2 0.48401 2.8833 0.1026

Interpretation:

First two lines tell us which models are being compared

Anova output

Analysis of Variance Table

Model 1: y ~ x3 + x4 + x6

Model 2: y ~ x2 + x3 + x4 + x5 + x6

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 1.32336

2 10 0.83935 2 0.48401 2.8833 0.1026

Interpretation:

\texttt{Res.Df} \, are the degrees of freedom of each model

The sample size of longley is 16

Model 1 has k=4 parameters

Model 2 has p=6 parameters

\mathop{\mathrm{df}}_1 = n - k = 16 - 4 = 12 \quad \qquad \mathop{\mathrm{df}}_2 = n - p = 16 - 6 = 10

Anova output

Analysis of Variance Table

Model 1: y ~ x3 + x4 + x6

Model 2: y ~ x2 + x3 + x4 + x5 + x6

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 1.32336

2 10 0.83935 2 0.48401 2.8833 0.1026

Interpretation:

\texttt{Df} \, is difference in degrees of freedom

\mathop{\mathrm{df}}_1 = 12 \mathop{\mathrm{df}}_2 = 10 Therefore the difference is

\mathop{\mathrm{df}}_1 - \mathop{\mathrm{df}}_2 = 12 - 10 = 2

Anova output

Analysis of Variance Table

Model 1: y ~ x3 + x4 + x6

Model 2: y ~ x2 + x3 + x4 + x5 + x6

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 1.32336

2 10 0.83935 2 0.48401 2.8833 0.1026

Interpretation:

\texttt{RSS} \, is the residual sum of squares for each model

\mathop{\mathrm{RSS}}_1 = 1.32336 \mathop{\mathrm{RSS}}_2 = 0.83935 \texttt{Sum of Sq} \, is the extra sum of squares

\mathop{\mathrm{RSS}}_1 - \mathop{\mathrm{RSS}}_2 = 0.48401

Anova output

Analysis of Variance Table

Model 1: y ~ x3 + x4 + x6

Model 2: y ~ x2 + x3 + x4 + x5 + x6

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 1.32336

2 10 0.83935 2 0.48401 2.8833 0.1026

Interpretation:

\texttt{F} \, is the F-statistic for model selection

\begin{align*}

F & = \frac{ \mathop{\mathrm{RSS}}_1 - \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{df}}_1 - \mathop{\mathrm{df}}_2 } \bigg/

\frac{ \mathop{\mathrm{RSS}}_2 }{ \mathop{\mathrm{df}}_2 } \\

& = \frac{ 1.32336 - 0.83935 }{ 12 - 10 } \bigg/

\frac{ 0.83935 }{ 10 } = 2.8833

\end{align*}

Anova output

Analysis of Variance Table

Model 1: y ~ x3 + x4 + x6

Model 2: y ~ x2 + x3 + x4 + x5 + x6

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 1.32336

2 10 0.83935 2 0.48401 2.8833 0.1026

Interpretation:

\texttt{Pr(>F)} is the p-value for F-test

F \, \sim \, F_{\mathop{\mathrm{df}}_1 - \mathop{\mathrm{df}}_2 , \, \mathop{\mathrm{df}}_2 } = F_{2, 10} Therefore the p-value is

p = P(F_{2,10} > F) = 0.1026

Anova output

Analysis of Variance Table

Model 1: y ~ x3 + x4 + x6

Model 2: y ~ x2 + x3 + x4 + x5 + x6

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 1.32336

2 10 0.83935 2 0.48401 2.8833 0.1026

Conclusion:

The p-value is p = 0.1026 > 0.05

This means we cannot reject H_0

Therefore the reduced Model 1 has to be preferred

This gives statistical evidence that X_2 and X_5 can be excluded from the model

GNP and Non-institutionalised do not affect Number of Employed

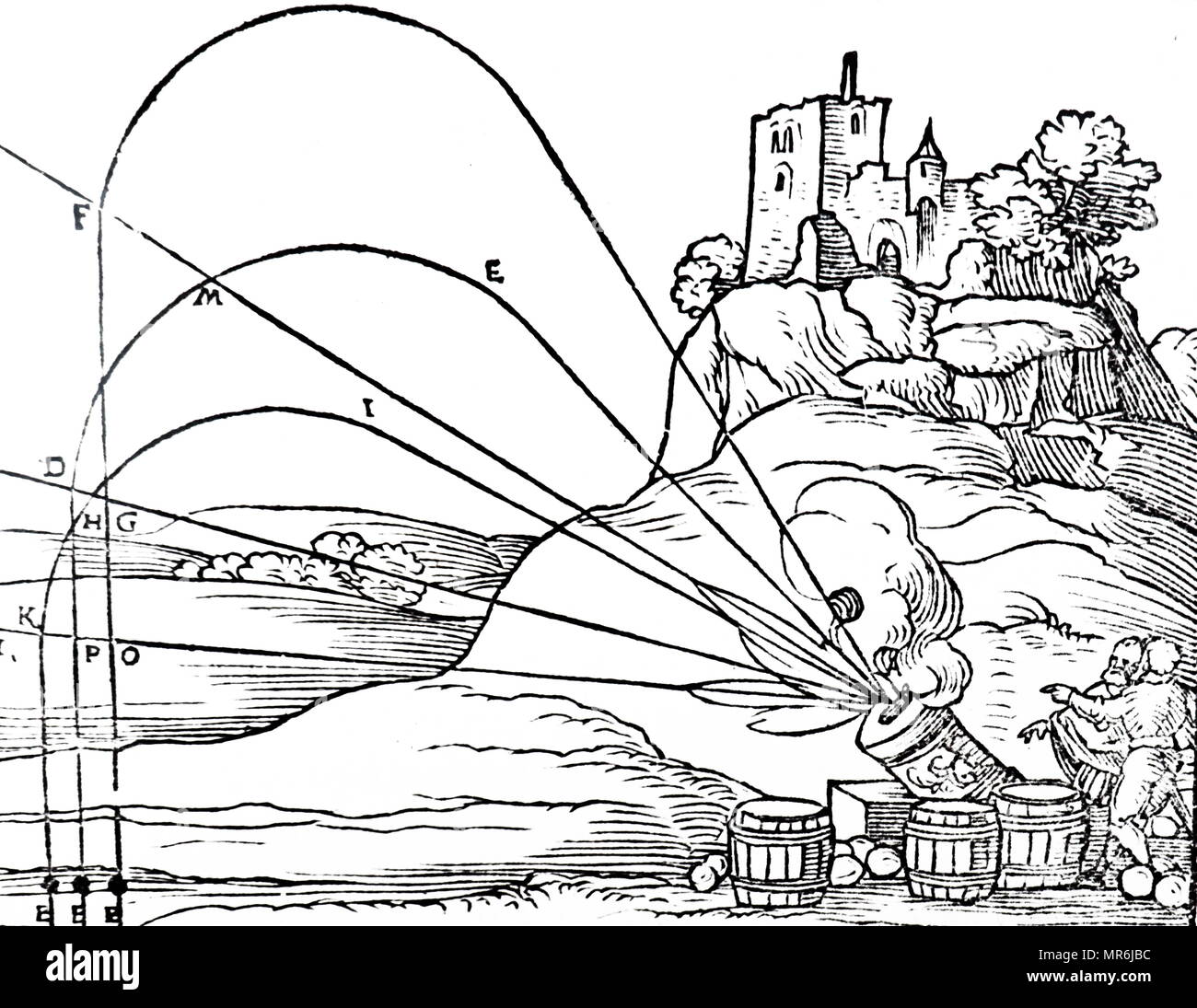

Example 2: Motion of falling bodies

Engraving (1546): people believed projectiles follow circular trajectories (source )

1609: Galileo proved mathematically that projectile trajectories are parabolic

His finding was based on empirical data

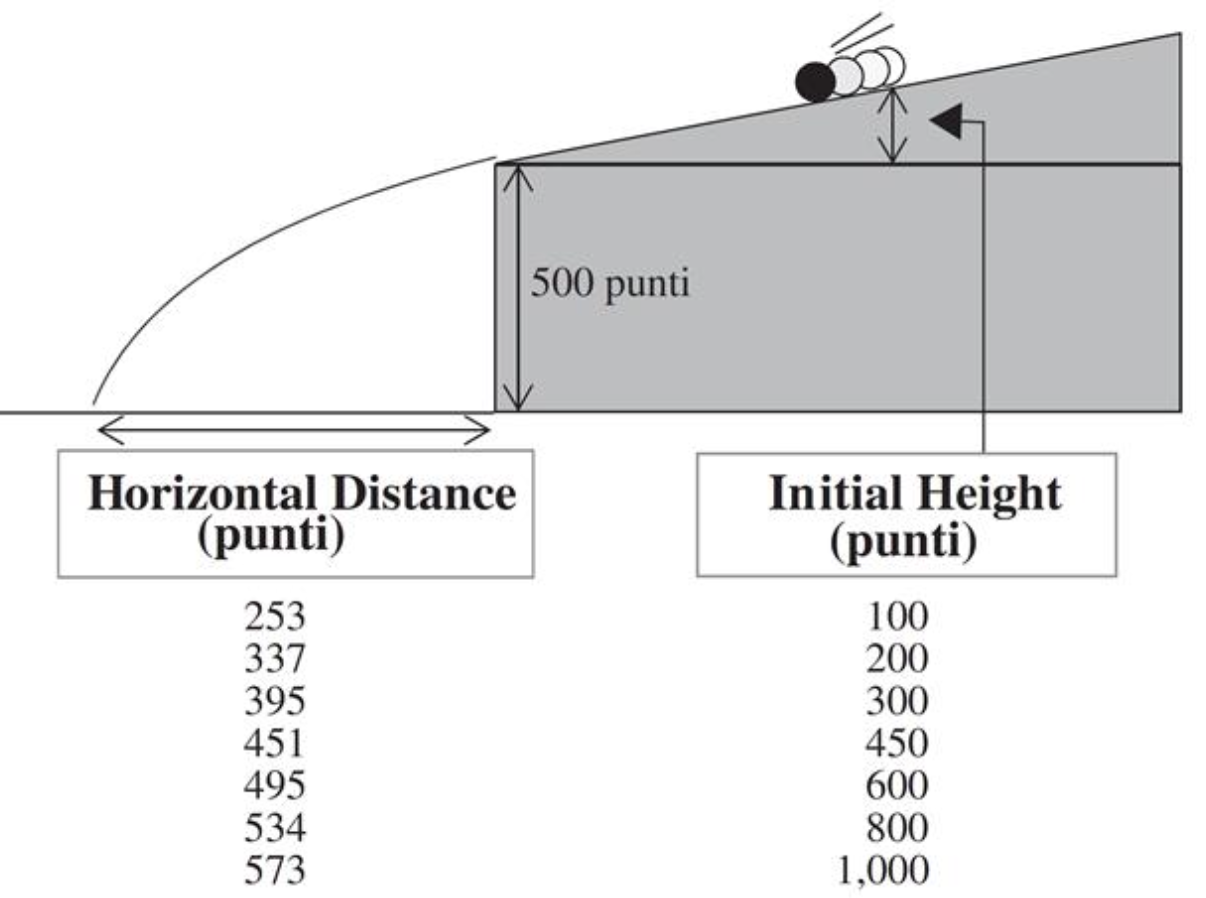

A ball (covered in ink) was released on an inclined plane from Initial Height

Ink mark on the floor represented the Horizontal Distance traveled

Unit of measure is punti \qquad\quad 1 \text{ punto} = 169/180 \, \text{mm}

We have access to Galileo’s original data [3 ]

Does a parabolic (quadratic) trajectory really explain the data?

Let’s fit a polynomial regression model and find out!

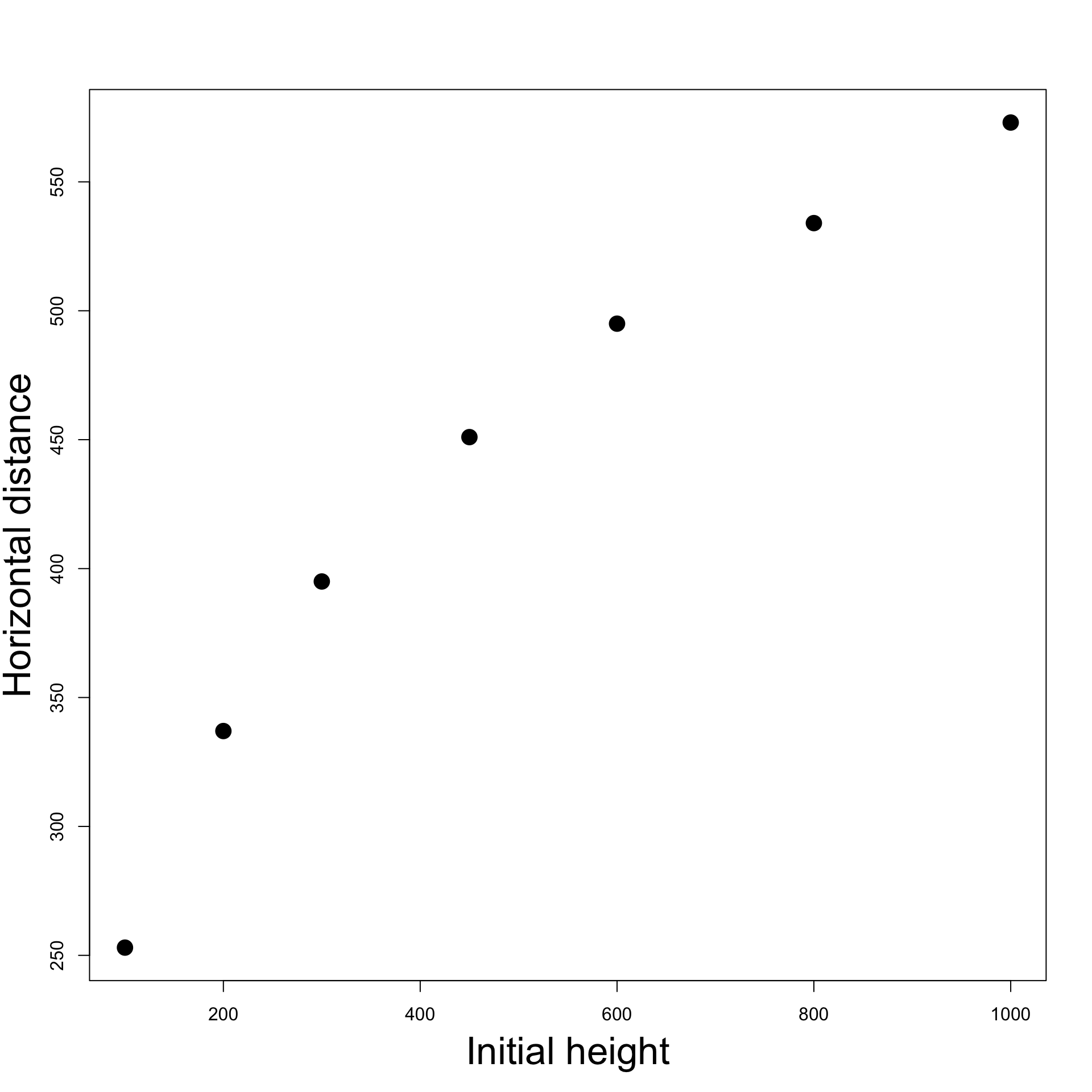

Plotting the data

Horizontal Distance 253

337

395

451

495

534

573

# Enter the data <- c (100 , 200 , 300 , 450 , 600 , 800 , 1000 )<- c (253 , 337 , 395 , 451 , 495 , 534 , 573 )# Scatter plot of data plot (height, distance, pch = 16 )

We clearly see a parabola. Therefore we expect a relation of the form

{\rm distance} = \beta_1 + \beta_2 \, {\rm height } + \beta_3 \, {\rm height }^2

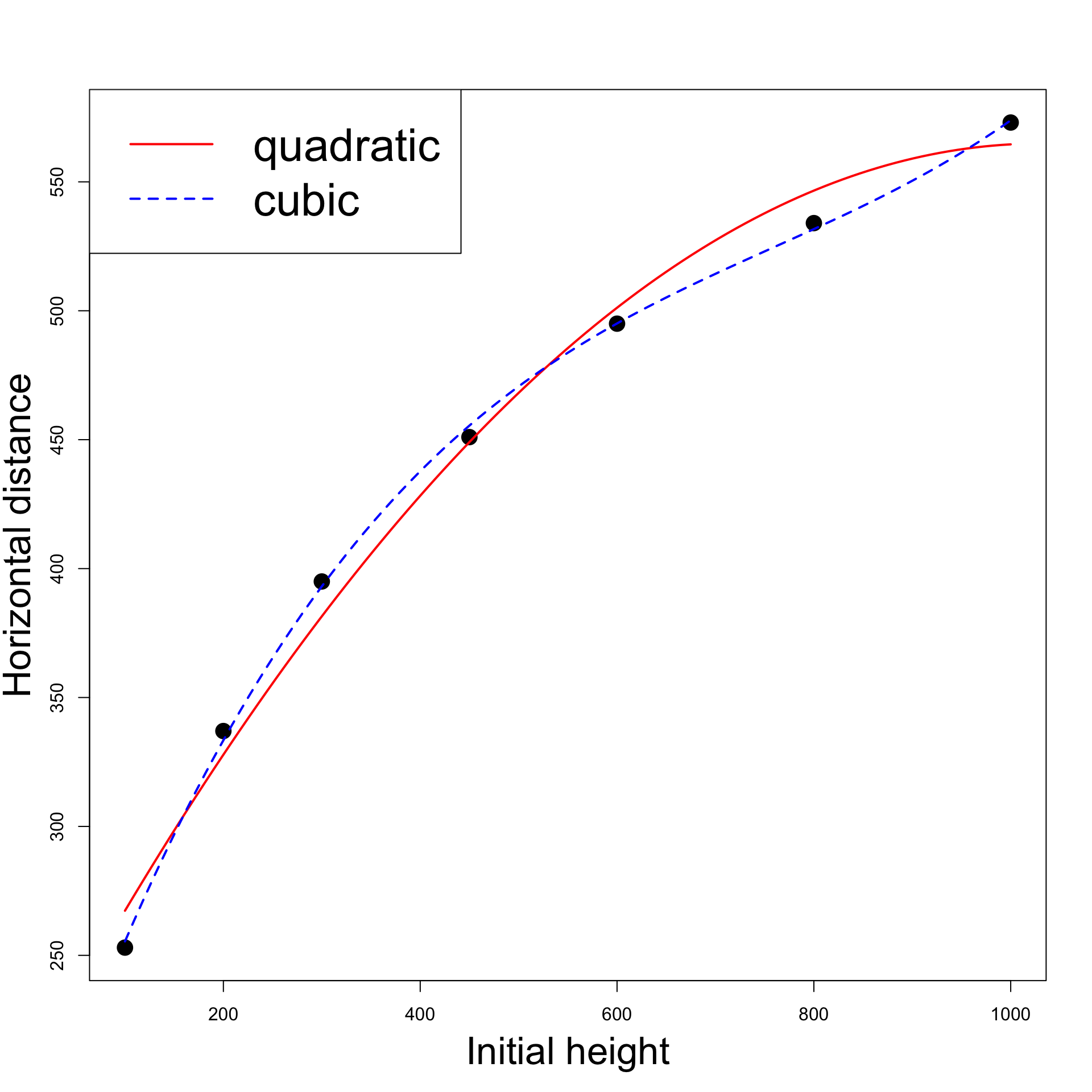

Fit linear model

{\rm distance} = \beta_1 + \beta_2 \, {\rm height }

# Fit linear model <- lm (distance ~ height)summary (linear)

Multiple R-squared: 0.9264, Adjusted R-squared: 0.9116

The coefficient of correlation is R^2 = 0.9264

R^2 is quite high, showing that a linear model fits reasonably well

Is a quadratic model better?

{\rm distance} = \beta_1 + \beta_2 \, {\rm height } + \beta_3

\, {\rm height }^2

Note: To specify powers we need to type \,\, \texttt{I}

# Fit quadratic model <- lm (distance ~ height + I ( height^ 2 ))summary (quadratic)

Multiple R-squared: 0.9903, Adjusted R-squared: 0.9855

The coefficient of correlation is R^2 = 0.9903

This is higher than the previous score R^2 = 0.9264

The quadratic trajectory explains 99\% of variability in the data

Why not try a cubic model?

{\rm distance} = \beta_1 + \beta_2 \, {\rm height } + \beta_3

\, {\rm height }^2 + \beta_4 \, {\rm height }^3

# Fit cubic model <- lm (distance ~ height + I ( height^ 2 ) + I (height^ 3 ))summary (cubic)

Multiple R-squared: 0.9994, Adjusted R-squared: 0.9987

The coefficient of correlation is R^2 = 0.9994

This is higher than the score of quadratic model R^2 = 0.9903

What is going on?

Quadratic vs cubic

# Model selection anova (quadratic, cubic, test = "F" )

Analysis of Variance Table

Model 1: distance ~ height + I(height^2)

Model 2: distance ~ height + I(height^2) + I(height^3)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 4 744.08

2 3 48.25 1 695.82 43.26 0.00715 **

Model selection: quadratic Vs cubic

\beta_4 = 0

Therefore the quadratic model does not describe the data well

The underlying relationship from Galileo’s data is cubic and not quadratic

Probably the inclined plane introduced drag

Code can be downloaded here galileo.R

Plot: Quadratic Vs Cubic

Click here for full code

# Enter the data <- c (100 , 200 , 300 , 450 , 600 , 800 , 1000 )<- c (253 , 337 , 395 , 451 , 495 , 534 , 573 )# Scatter plot of data plot (height, distance, xlab = "" , ylab = "" , pch = 16 , cex = 2 )# Add labels mtext ("Initial height" , side = 1 , line = 3 , cex = 2.1 )mtext ("Horizontal distance" , side = 2 , line = 2.5 , cex = 2.1 )# Fit quadratic model <- lm (distance ~ height + I ( height^ 2 ))# Fit cubic model <- lm (distance ~ height + I ( height^ 2 ) + I (height^ 3 ))# Plot quadratic Vs Cubic <- Vectorize (function (x, ps) {<- length (ps)sum (ps* x^ (1 : n-1 ))"x" )curve (polynomial (x, coef (quadratic)), add= TRUE , col = "red" , lwd = 2 )curve (polynomial (x, coef (cubic)), add= TRUE , col = "blue" , lty = 2 , lwd = 2 )legend ("topleft" , legend = c ("quadratic" , "cubic" ), col = c ("red" , "blue" ), lty = c (1 ,2 ), lwd = 2 , cex = 2.5 )

Why not try higher degree polynomials

{\rm distance} = \beta_1 + \beta_2 \, {\rm height } + \beta_3

\, {\rm height }^2 + \beta_4 \, {\rm height }^3

+ \beta_5 \, {\rm height }^4

# Fit quartic model <- lm (distance ~ height + I ( height^ 2 ) + I (height^ 3 ) + I (height^ 4 ))summary (quartic)

Multiple R-squared: 0.9998, Adjusted R-squared: 0.9995

We obtain a coefficient R^2 = 0.9998

This is even higher than cubic model coefficient R^2 = 0.9994

Is the quartic model actually better?

Model selection: cubic Vs quartic

# Model selection anova (cubic, quartic, test = "F" )

Analysis of Variance Table

Model 1: distance ~ height + I(height^2) + I(height^3)

Model 2: distance ~ height + I(height^2) + I(height^3) + I(height^4)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 3 48.254

2 2 12.732 1 35.522 5.5799 0.142

The F-test is not significant since p = 0.142 > 0.05

This means we cannot reject the null hypothesis that \beta_5 = 0

The cubic models does better than quartic, despite higher R^2

The underlying relationship from Galileo’s data is indeed cubic!

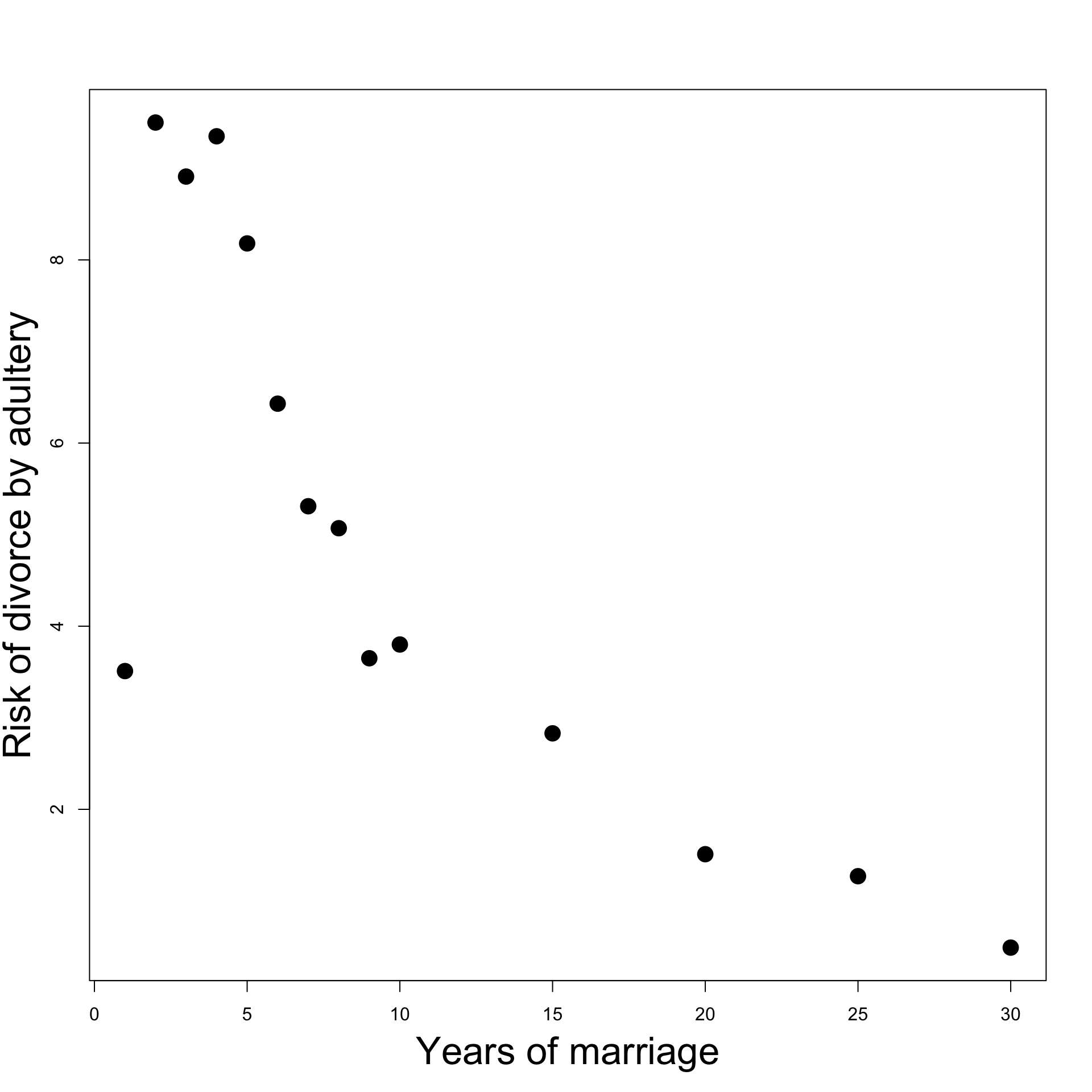

Example 3: Divorces

Data from Daily Mirror gives

Percentage of divorces caused by adultery VS years of marriage

Original analysis claimed

Divorce-risk peaks at year 2 then decreases thereafter

Is this conclusion misleading?

Does a quadratic model offers a better fit than a straight line model?

Divorces dataset

Percent of divorces caused by adultery by year of marriage

% divorces adultery 3.51

9.50

8.91

9.35

8.18

6.43

5.31

% divorces adultery 5.07

3.65

3.80

2.83

1.51

1.27

0.49

Plot: Years of Marriage Vs Divorce-risk

Looks like: Divorce-risk is

First low,

then peaks at year 2

then decreases

Change of trend suggests:

Higher order model might be good fit

Consider quadratic model

Click here for full code

# Divorces data <- c (1 , 2 , 3 , 4 , 5 , 6 ,7 , 8 , 9 , 10 , 15 , 20 , 25 , 30 )<- c (3.51 , 9.5 , 8.91 , 9.35 , 8.18 , 6.43 , 5.31 , 5.07 , 3.65 , 3.8 , 2.83 , 1.51 , 1.27 , 0.49 )# Scatter plot of data plot (year, percent, xlab = "" , ylab = "" , pch = 16 , cex = 2 )# Add labels mtext ("Years of marriage" , side = 1 , line = 3 , cex = 2.1 )mtext ("Risk of divorce by adultery" , side = 2 , line = 2.5 , cex = 2.1 )

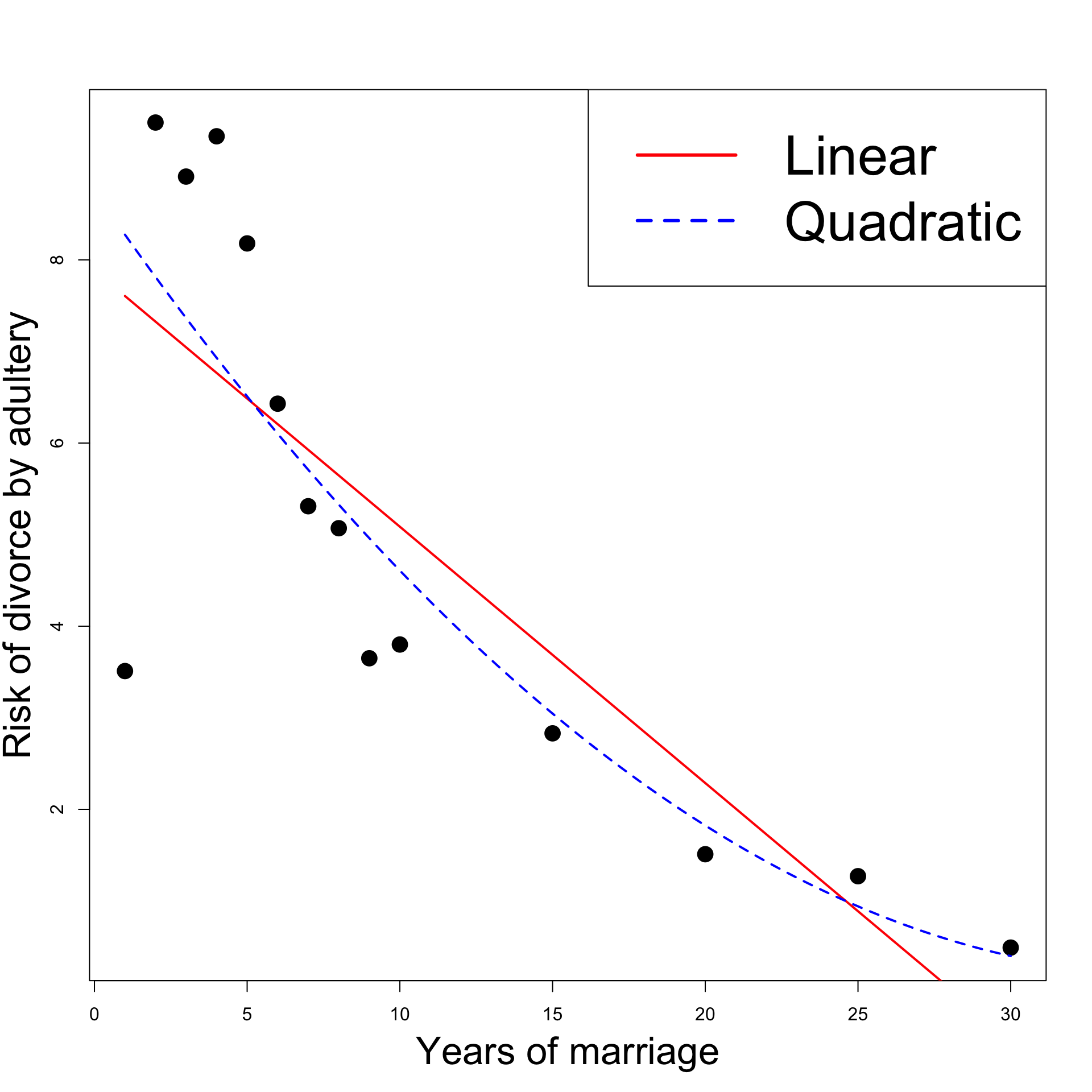

Fitting linear model

# Divorces data <- c (1 , 2 , 3 , 4 , 5 , 6 ,7 , 8 , 9 , 10 , 15 , 20 , 25 , 30 )<- c (3.51 , 9.5 , 8.91 , 9.35 , 8.18 , 6.43 , 5.31 , 5.07 , 3.65 , 3.8 , 2.83 , 1.51 , 1.27 , 0.49 )# Fit linear model <- lm (percent ~ year)summary (linear)

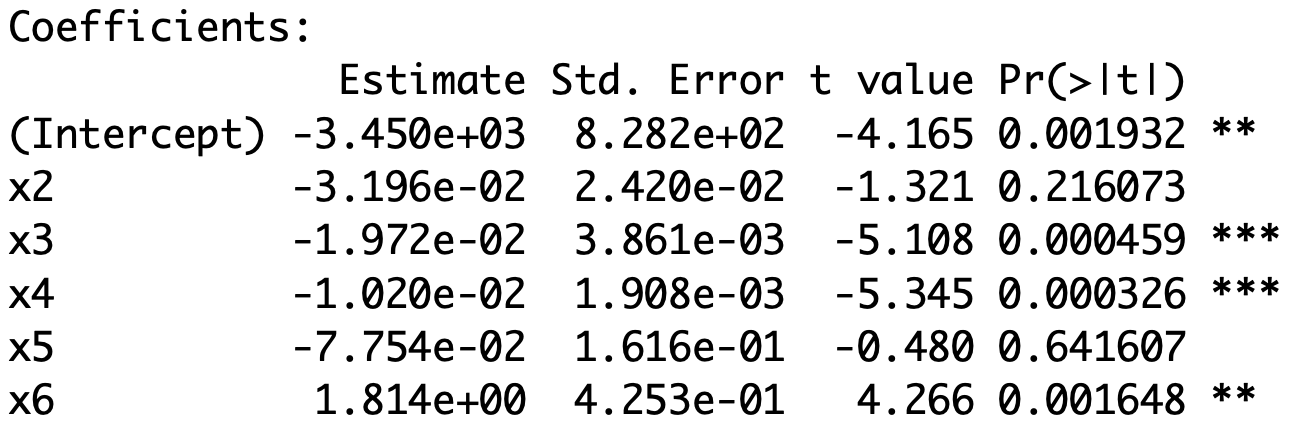

Estimate Std. Error t value Pr(>|t|)

(Intercept) 7.88575 0.78667 10.024 3.49e-07 ***

year -0.27993 0.05846 -4.788 0.000442 ***

t-test for \beta_2 is significant since p = 0.0004 < 0.05

Therefore \beta_2 \neq 0 and the estimate is \hat \beta_2 = -0.27993

The risk of divorce decreases with years of marriage (because \hat \beta_2 < 0 )

Fitting quadratic model

# Fit quadratic model <- lm (percent ~ year + I ( year^ 2 ))summary (quadratic)

Estimate Std. Error t value Pr(>|t|)

(Intercept) 8.751048 1.258038 6.956 2.4e-05 ***

year -0.482252 0.235701 -2.046 0.0654 .

I(year^2) 0.006794 0.007663 0.887 0.3943

t-test for \beta_3 is not significant since p = 0.3943 > 0.05

Cannot reject null hypothesis \beta_3 = 0 \quad \implies \quad Quadratic term not needed!

The original analysis in the Daily Mirror is probably mistaken

Model selection: Linear Vs Quadratic

# Model selection anova (linear, quadratic, test = "F" )

Model 1: percent ~ year

Model 2: percent ~ year + I(year^2)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 42.375

2 11 39.549 1 2.826 0.786 0.3943

F-test is not significant since p = 0.3943 > 0.05

We cannot reject the null hypothesis that \beta_3 = 0

Quadratic model is worse than linear model

Conclusions

Daily Mirror Claim: Divorce-risk peaks at year 2 then decreases thereafter

Claim suggests higher order model needed to explain change in trend

Analysis conducted:

Fit linear and quadratic regression models

t-test of significance discarded quadratic term

F-test for model selection discarded Quadratic model

Findings: Claims in Daily Mirror are misleading

Linear model seems to be better than quadratic

This suggests divorce-risk generally decreases over time

Peak in year 2 can be explained by unusually low divorce-risk in 1st year

Code is available here divorces.R

Click here for full code

# Divorces data <- c (1 , 2 , 3 , 4 , 5 , 6 ,7 , 8 , 9 , 10 , 15 , 20 , 25 , 30 )<- c (3.51 , 9.5 , 8.91 , 9.35 , 8.18 , 6.43 , 5.31 , 5.07 , 3.65 , 3.8 , 2.83 , 1.51 , 1.27 , 0.49 )# Fit linear model <- lm (percent ~ year)# Fit quadratic model <- lm (percent ~ year + I ( year^ 2 ))# Scatter plot of data plot (year, percent, xlab = "" , ylab = "" , pch = 16 , cex = 2 )# Add labels mtext ("Years of marriage" , side = 1 , line = 3 , cex = 2.1 )mtext ("Risk of divorce by adultery" , side = 2 , line = 2.5 , cex = 2.1 )# Plot Linear Vs Quadratic <- Vectorize (function (x, ps) {<- length (ps)sum (ps* x^ (1 : n-1 ))"x" )curve (polynomial (x, coef (linear)), add= TRUE , col = "red" , lwd = 2 )curve (polynomial (x, coef (quadratic)), add= TRUE , col = "blue" , lty = 2 , lwd = 2 )legend ("topright" , legend = c ("Linear" , "Quadratic" ), col = c ("red" , "blue" ), lty = c (1 ,2 ), cex = 3 , lwd = 3 )

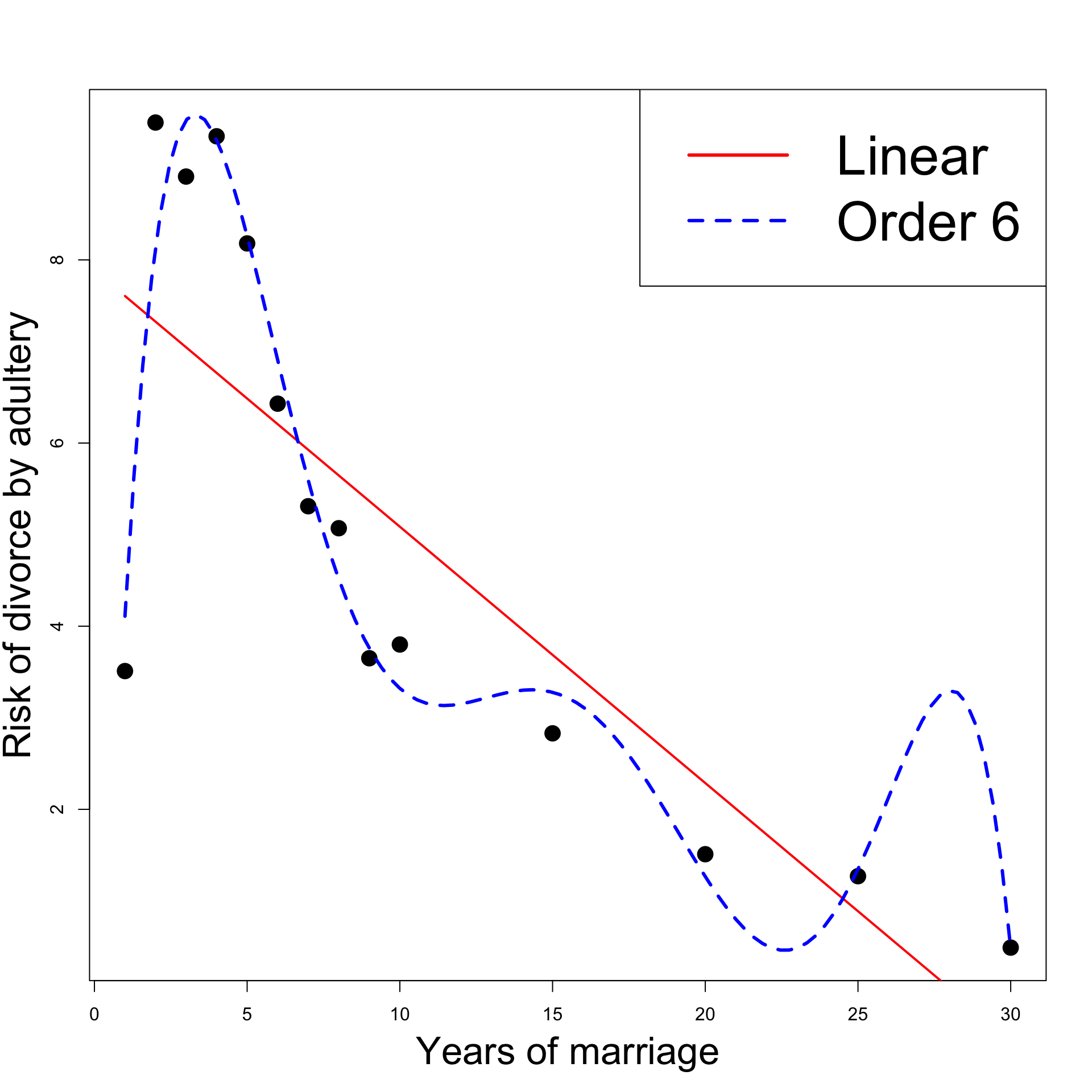

Why not try higher order polynomials

Let us compare Linear model with Order 6 Model

# Fit order 6 model <- lm (percent ~ year + I ( year^ 2 ) + I ( year^ 3 ) + + I ( year^ 4 ) + I ( year^ 5 ) + + I ( year^ 6 ))# Model selection anova (linear, order_6)

Model 1: percent ~ year

Model 2: percent ~ year + I(year^2) + I(year^3) + I(year^4) + I(year^5) +

+I(year^6)

Res.Df RSS Df Sum of Sq F Pr(>F)

1 12 42.375

2 7 3.724 5 38.651 14.531 0.001404 **

Why not try higher order polynomials

\beta_3 = \beta_4 = \beta_5 = \beta_6 = 0

The Order 6 model is better than the Linear model

Peak divorce-rate in Year 2 is well explained by order 6 regression

What is going on? Let us plot the regression functions

There are more peaks:

Decreasing risk of divorce for 23 years

But it gets boring after 27 years!

Model overfits :

Data is very well explained

but predictions are not realistic

Linear model should be preferred

Click here for full code

# Divorces data <- c (1 , 2 , 3 , 4 , 5 , 6 ,7 , 8 , 9 , 10 , 15 , 20 , 25 , 30 )<- c (3.51 , 9.5 , 8.91 , 9.35 , 8.18 , 6.43 , 5.31 , 5.07 , 3.65 , 3.8 , 2.83 , 1.51 , 1.27 , 0.49 )# Fit linear model <- lm (percent ~ year)# Fit order 6 model <- lm (percent ~ year + I ( year^ 2 ) + I ( year^ 3 ) + I ( year^ 4 ) + I ( year^ 5 ) + I ( year^ 6 ))# Scatter plot of data plot (year, percent, xlab = "" , ylab = "" , pch = 16 , cex = 2 )# Add labels mtext ("Years of marriage" , side = 1 , line = 3 , cex = 2.1 )mtext ("Risk of divorce by adultery" , side = 2 , line = 2.5 , cex = 2.1 )# Plot Linear Vs Quadratic <- Vectorize (function (x, ps) {<- length (ps)sum (ps* x^ (1 : n-1 ))"x" )curve (polynomial (x, coef (linear)), add= TRUE , col = "red" , lwd = 2 )curve (polynomial (x, coef (order_6)), add= TRUE , col = "blue" , lty = 2 , lwd = 3 )legend ("topright" , legend = c ("Linear" , "Order 6" ), col = c ("red" , "blue" ), lty = c (1 ,2 ), cex = 3 , lwd = 3 )